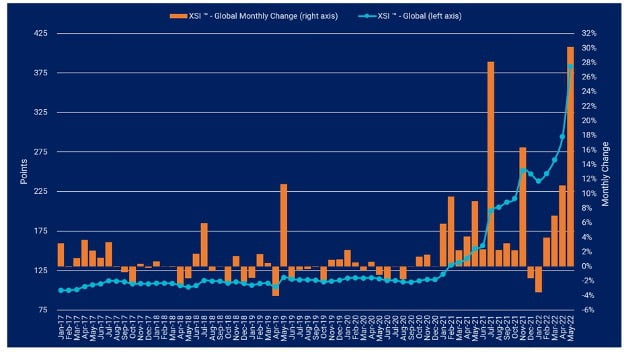

The global XSI ® jumped by an unprecedented 30.1% in May to 383.12 points. Since the end of 2021, the index has appreciated by 55.0%. ▶︎ Global Index ▶︎ Far East Indices (Import/Export) ▶︎ Europe Indices (Import/Export) ▶︎ US Indices (Import/Export)

The global XSI ® jumped by an unprecedented 30.1% in May to 383.12 points. The month-on-month rise is the largest on record and takes the benchmark to 150.6% higher than this time last year. Since the end of 2021, the index has appreciated by 55.0%.

In May the global XSI ® registered 383.12 points, its highest ever level and 150.6% higher than this time last year. Month-on-month the index increased by an unprecedented 30.1% in May, as older, long-term contracts signed with much lower rates have now almost entirely been replaced by newer ones at much higher levels. Since the end of 2021, the index has appreciated by 55.0%.

Reflecting the increase, Israeli carrier Zim posted a 113% year-on-year jump in revenue for the last quarter. EBITDA for Q1 was recorded at $2.5bn, whilst a new record for net profit was reported at $1.7bn.

Due to its impressive results, the carrier has upgraded its full-year EBITDA guidance to $7.8bn- $8.2bn. The strategy of limiting its contract business, whilst launching additional services in high-demand markets, seems to have paid off. However, even for its contracted business, Zim noted that rates on the transpacific were more than double where they were in the previous year.

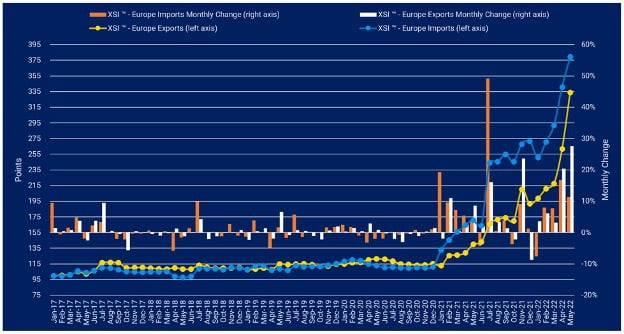

European imports on the XSI ® continued to reach fresh all-time highs after increasing by 11.3% to 379.13 points.

Year-on-year the index is now up by 122.0% and had risen by 39.7% since Dec-21.

Exports also rose in May, jumping by 27.6% to 333.91. This month-on-month increase is the largest ever reported and takes the index to 138.3% higher than the equivalent period last year.

Since the end of 2021, the benchmark has risen by 74.1%.

The increase in both indexes reflects the rise in the average long-term rate of all long-term contracts currently valid and therefore what shippers are paying.

Those currently looking to sign long-term contracts will find some relief in flat, and in some cases softening rates month-on-month.

Whilst rates in the spot market on the key Far East-North Europe trades have softened in recent months, the declines have slowed following a series of blanked sailings from carriers.

However, carriers will be well aware of the increasing scrutiny they face following the dramatic rise in rates and will not want to provide any signs of unfair practices.

Regulators from China, Europe and the US have all made it clear they could increase the scope of the investigations into carrier practices, albeit so far, they have failed to find any evidence of unfair competition.

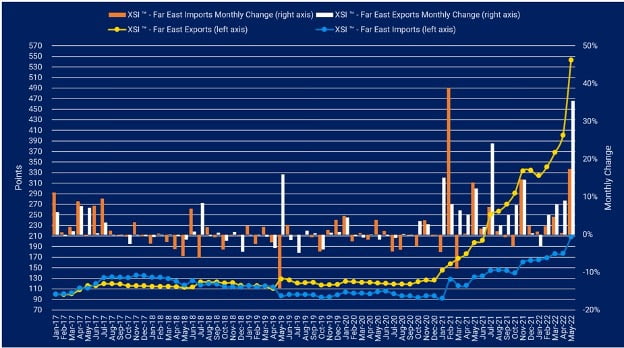

Far East imports on the XSI ® jumped by 17.4% in May-22 to 207.99.

This represents one of the largest month-on-month increases on record and takes the index to 57.1% higher than in May-21, as older contracts with lower rates have now almost entirely been replaced by the new round of contracts with much higher rates. Since the end of last year, the index has risen by 26.9%.

Meanwhile, exports increased by 35.4% to 542.79. The increase was the largest reported since the inception of the index and means it is now up by 174.8% year-on-year. Since Dec-21 the benchmark has appreciated by 62.5%.

In Shanghai, the end of lockdown is in sight, with restrictions being lifted next month. Whilst a positive development, there are concerns that a lack of cargo moved during this period due to blanked sailings, could cause further disruption as the market enters peak season.

Elsewhere, the impact of a zero COVID policy is now being reflected by China’s National Bureau of Statistics (NBS). Figures released for April show a 4.6% reduction in manufacturing output and a fall of 2.8% for industrial output.

It now seems highly unlikely the country can maintain its aim of annual GDP growth of 5.5%, with some even predicting a contraction in Q2.

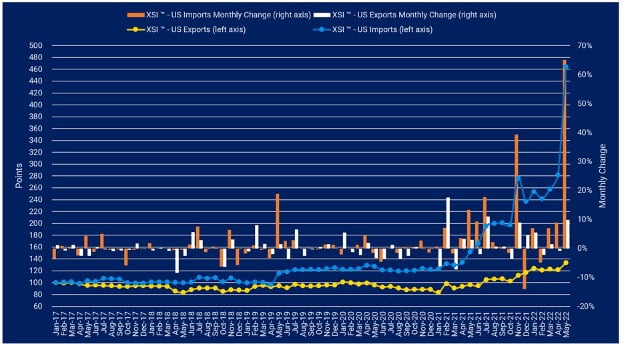

US imports on the XSI ® skyrocketed by 65.1% in May to 464.09 points, its highest ever level as only very few shippers are still enjoying rates that would have been considered ‘normal’ a few years ago. With this latest rise, the benchmark is now 205.4% higher than this time last year and has risen by 95.9% since the end of 2021.

Whilst less dramatic, exports also rose this month, increasing by 9.9% to 133.7. Compared to the equivalent period of 2021, the index has appreciated by 38.5% and has risen by 14.1% since the end of last year.

The recent lockdown in Shanghai has also been reflected in throughput volumes at major terminals. In Los Angeles, recent weekly throughput was down by 31% year-on-year, albeit this had a positive effect on berth waiting times, which dropped to just 1.2 days from an average of 15 recorded prior to the lockdown.