Long-term contracted ocean freight rates climbed by 7% in March. ▶︎ Global Index ▶︎ Far East Indices (Import/Export) ▶︎ Europe Indices (Import/Export) ▶︎ US Indices (Import/Export)

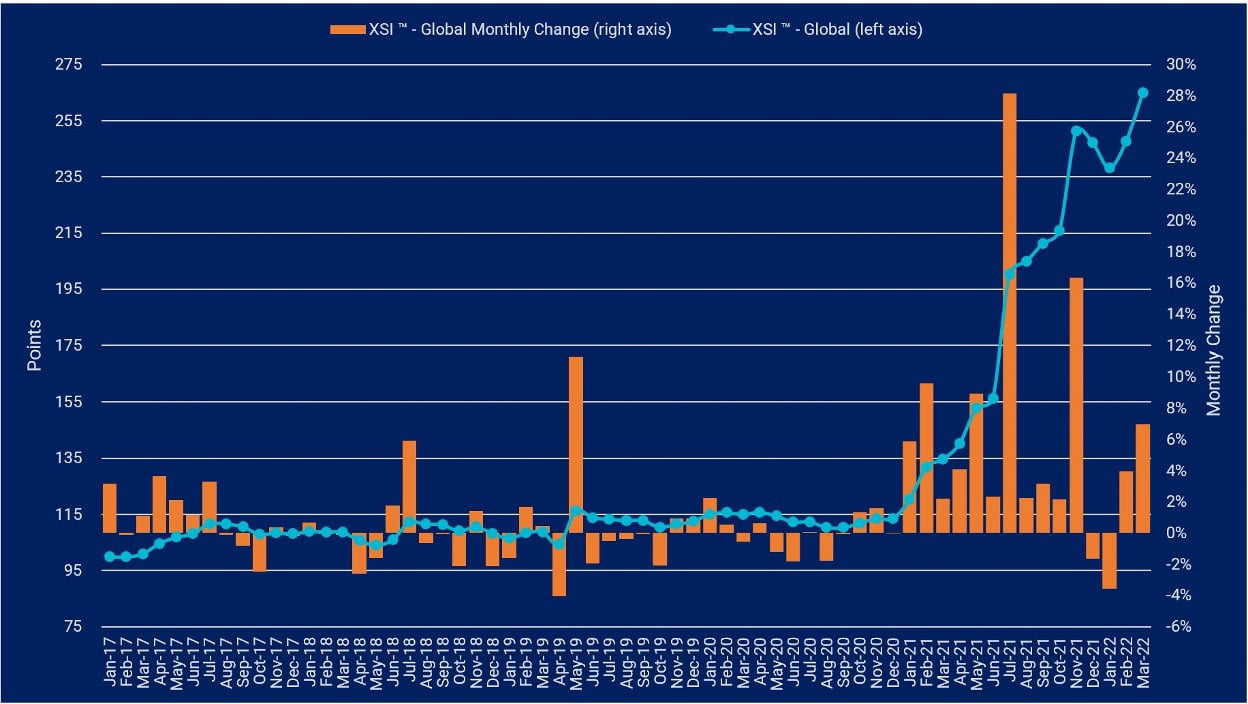

The global XSI ® continued to climb in March 2022, rising by 7.0% month-on-month to 265.0 points.

This represents a new all-time high for the benchmark and ensures the index is 96.7% higher than the equivalent period of 2021. It has also appreciated by 7.2% since the end of last year.

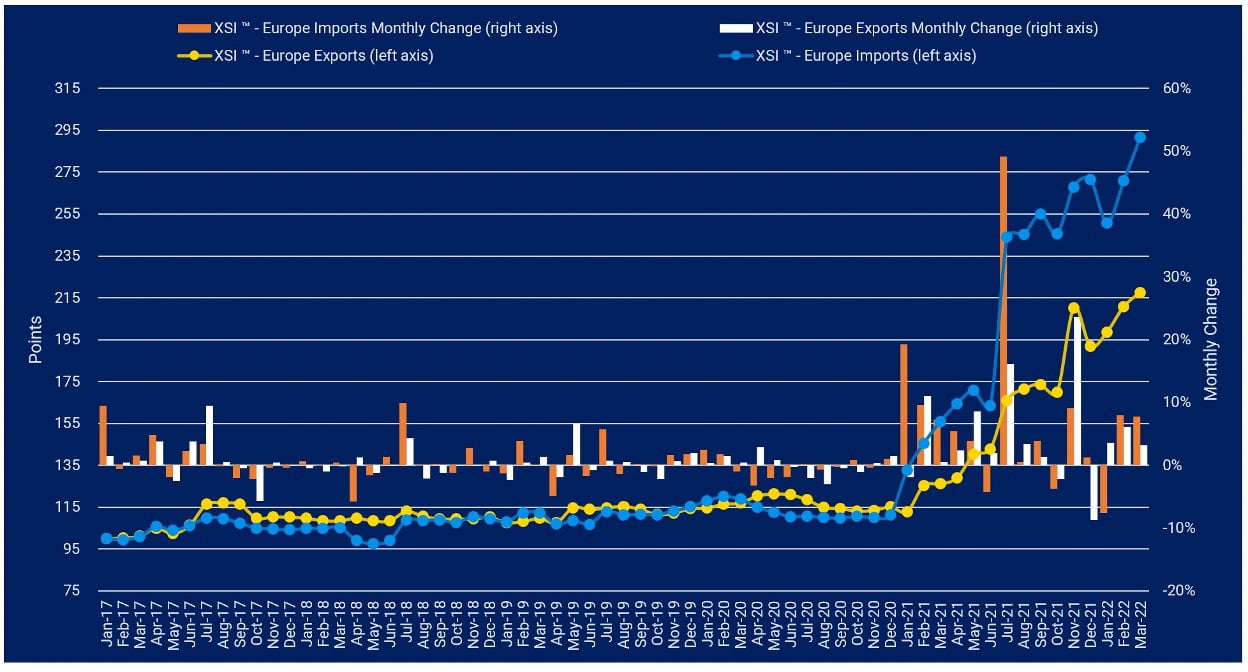

European imports on the XSI ® rose by 7.7% in Mar-22 to 291.72. Representing a new all-time high, the index has continued to climb despite spot rates softening recently on the Far East-North Europe trade.

Year-on-year, the benchmark is up by 87.1%, and it is 7.5% higher than in Dec-21. Exports also continued to climb in March, rising by 3.2% to 217.52 points. While growth on the exports index has been less extreme than the increases seen for imports, the benchmark is still at an all-time high.

It has also increased by 72.5% year-on-year and is 13.4% higher than in 2021. With rates on the key Far East - Europe trades declining, carriers are in the process of blanking sailings to combat sluggish demand. Maersk and MSC recently announced plans to void three additional sailings next month due to what they described as a challenging market situation.

This has been partly attributed to the recent week-long shutdown of Shenzhen, resulting in a flurry of canceled bookings. However, in the last few years, rates have become weaker in the month following the Chinese New Year, and therefore it may just be a temporary blip. The declines do, however, highlight how volatile rates can be, and with Covid still rearing its head, combined with China's strict lockdown policy, there is the potential for additional shutdowns and subsequent falls in demand.

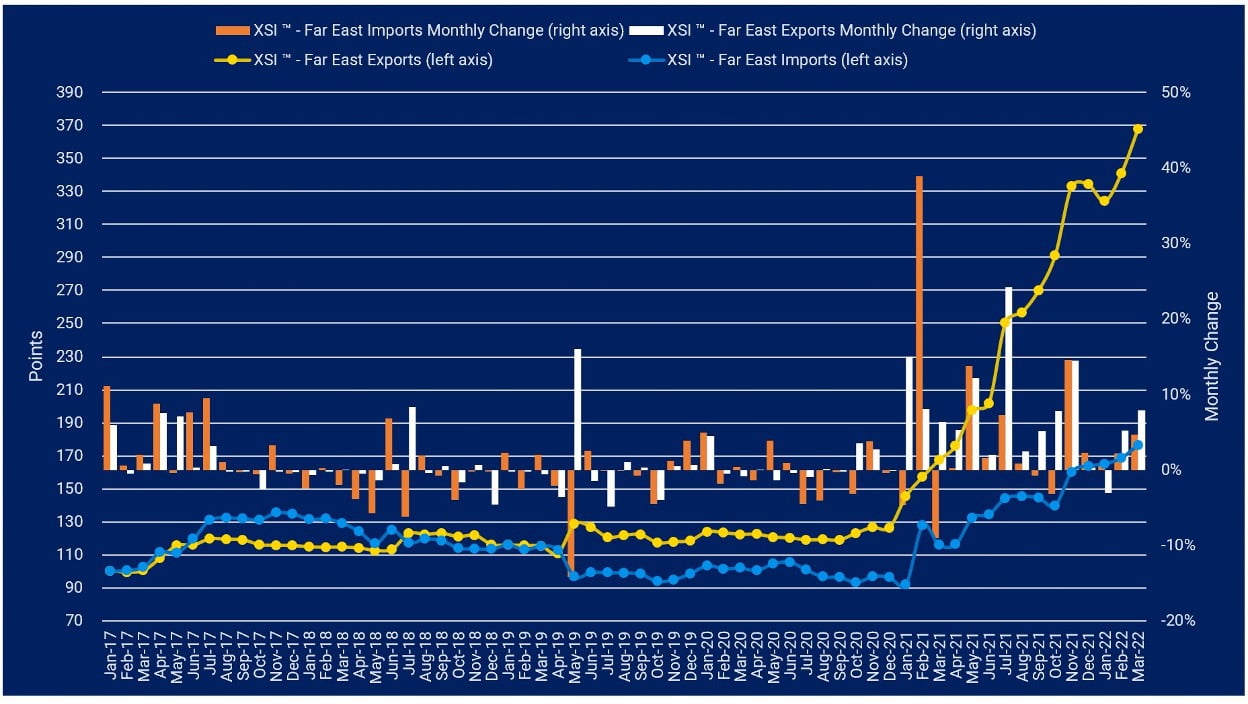

Far East imports on the XSI ® jumped by 4.7% in March to 176.52 points. The benchmark is now 52.1% higher than the same period last year and has risen by 7.7% since Dec-21.

Although increases have been less severe than on the export element of the index, it has been steadily increasing since the all-time low of 91.93 reported in Jan-21 and is now up by 92.0%.

Exports also rose this month, increasing by 7.9% to 367.88. Whilst the index saw a temporary blip in January this year, over the last 24 months it has increased 18 times, highlighting how upwards momentum has been sustained since the onset of the pandemic.

Year-on-year the index is up by 120.0% and has increased by 10.1% since the end of 2021. In further signs of the windfall, carriers are experiencing, Evergreen’s latest financial results show that the company’s revenue jumped to $17.67bn. President Eric Hsieh expects rates to remain elevated for the rest of the year with bumper profits likely to continue.

Off the back of this and like other lines, Evergreen will be expanding its capacity in the years ahead and could take delivery of more than 40 new vessels by the end of 2025, totaling more than 550,000 TEU.

Whether this additional capacity will be met by demand is open for debate, but without the ability to adequately hedge the revenue risk associated with this additional capacity, the market could again go from boom to bust unless fundamentals remain in their favor.

Yet again we saw another bumper month for the carrier community, with climbs across all major trade corridors, for both export and import indices. Long-term rates are reaching all-time highs, and carriers are undoubtedly sitting pretty in contract negotiations, but there are signs that future adjustments may be edging onto the horizon.

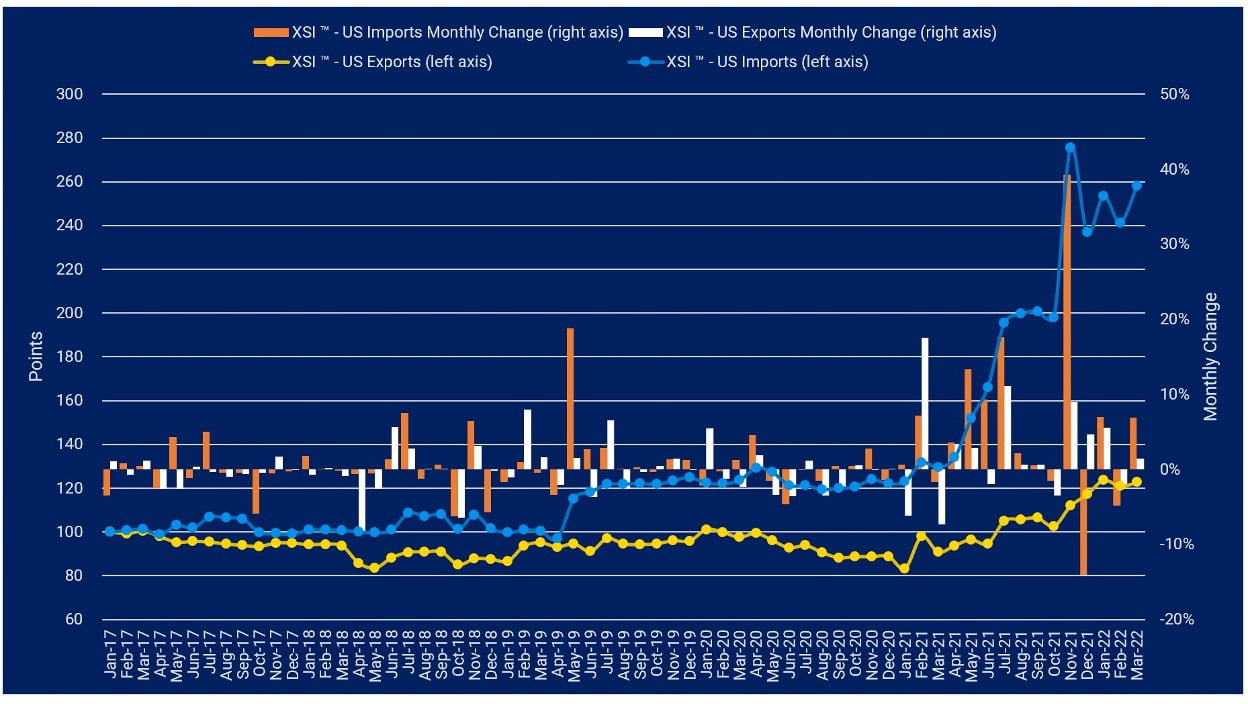

US imports on the XSI ® rose by 6.9% in March to 258.04 points. This month-on-month increase more than offset the decline reported in February.

The index is now 99.3% higher than the equivalent period of 2021 and has risen by 8.9% since the end of last year. Exports also increased this month, albeit to a lesser extent. The benchmark appreciated by 1.4% to 122.69 and is up by 35.2% year-on-year. Since Dec-21 the index has risen by 4.7%.

In a positive sign for shippers, average waiting times at Los Angeles and Long Beach have improved after carriers decided to shift some operations to US east coast ports.

Some facilities are even reporting no noticeable delays. Furthermore, in the medium-term, potential Covid related shutdowns in Asia and rising inflation could lead to a reduction in demand, which could improve the situation further.