Q3 2023

MACROECONOMICS

Quarterly overview of the majordevelopments on the macroeconomic landscape

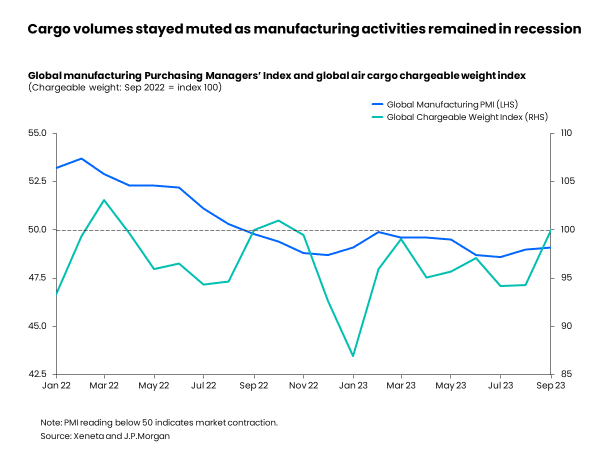

Global manufacturing continued to struggle in the third quarter of this year, with data from the latest manufacturing Purchasing Managers’ Index (PMI) showing the 13th consecutive month-on-month contraction in September.

A PMI reading below the threshold 50.0 mark indicates the contraction in manufacturing activities. But this deterioration has slowed down with an improved reading in the last two months.

A key indicator of global trade and air cargo activity is the manufacturing PMI’s subindex for new export orders, which reflects expected future exports.

In September, the global new export orders subindex was 47.7, registering a 19-month consecutive contraction. But it was at a slower rate than in August, when it was 47.0.

The decline in global new export orders was in line with market sentiment. Plagued by the prospect of high interest rates, US annual inflation dropped to 3.7% year-on-year in September when measured by the consumer price index (CPI). Although major progress has been made from the peak of 9.1% in June 2022, it remained higher than the Fed’s target of 2%.

Germany, the EU’s largest economy, showed a similar trend. Its CPI fell to 4.5% in September, but still higher than the EU’s 2% inflation target. Generally speaking, inflation is higher in European economies than the US and other countries around the world largely due to increased energy prices as a result of the war in Ukraine.

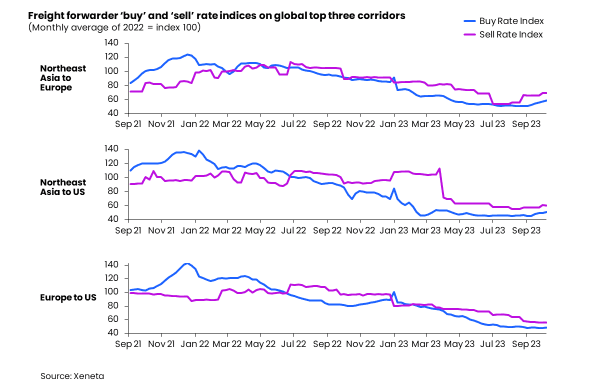

High inflation is likely to weigh on consumer spending and, subsequently, retail sales. In August retail sales in the US and EU grew 2.0% and 3.3% year-on-year respectively, but when adjusted for inflation both retail sales growth ratios fell below last year’s levels. The rising inflationary pressures and the tightening of monetary policy by central banks haseroded consumer and business confidence and reduced the demand for goods.

This is hurting the air freight market because consumers shift their spending from expensive durable goods to essentials, which to some extent also explains the steady demand seen in the air special cargo market.

Consequently, the volume of global merchandise trade volume is expected to grow by a meager 0.8% in 2023, according to the latest October release from the World Trade Organization (WTO). This is a significant downward revision from the 1.7% forecast made in April.

Despite the growth in global trade, air freight volumes look set to be subdued again this year. The shift towards spending on essential goods means the goods typically transported by air are seeing weak demand.

Conflict has disrupted air freight transportation in and out of the region, with several airlines cancelling their flights to Tel Aviv due to security reasons. The air freight market will likely be impacted as charter services will be arranged to fill gaps in cancelled scheduled flights and further exposure through war-risk related insurance surcharges. However, the impact is unlikely to spread beyond this region.

Another consequence of this conflict is price increases in crude oil and natural gas. Crude oil price rose 4% week-on-week in mid-October. But as the region is not a major oil producing region, this trend will likely not be long term, provided the conflict does not spread to involve major oil producing nations such as Iran.

Increased natural gas prices following the shutdown of a gas field in Israel and damage to a gasoline pipeline between Finland and Estonia may add to inflationary pressures in Europe.