RATES

Air Freight

Quarterly overview of the majordevelopments in air freight rates

Ocean shipping chaos driving up airline rates

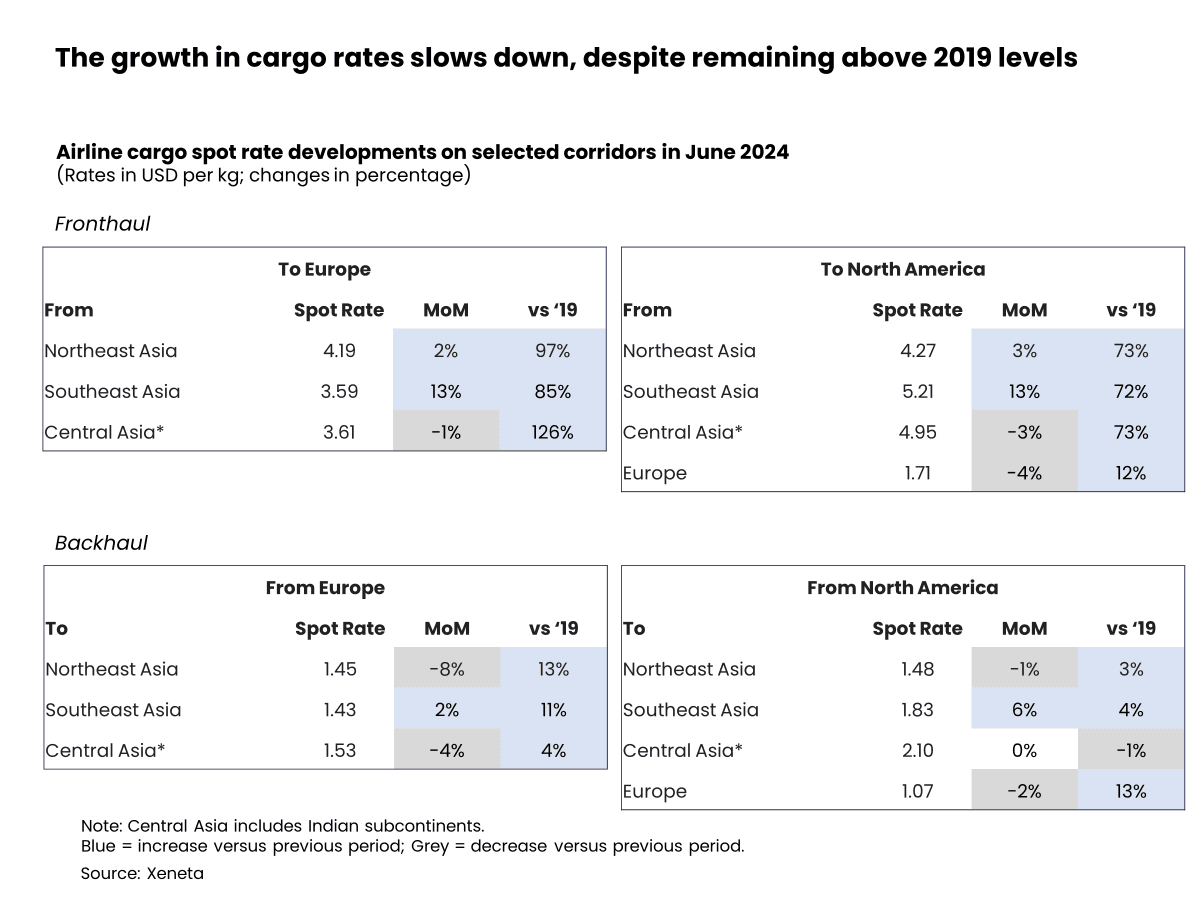

As the market ended the first half of 2024, global air cargo rates remained elevated following an initial peak in early April.

While backhaul corridors were nearing pre-pandemic levels, outbound Asia airline spot rates continued to face upward pressure in the near term.

The turmoil in the ocean container shipping sector is a key contributor to the air cargo market surge. Therefore, examining the ocean container market may offer insights into future air cargo market trends.

Currently, ex Asia container spot rates are heading towards the second peak since having reached an initial peak Red Sea crisis peak in late January/early February before softening slightly in March and April.

The scale of the increases in ocean spot rates on trades out of the Far East since the beginning of May is the largest when tracking rate developments since 2018.

The 40ft dry container spot rate from the Far East to North Europe grew by 99% in late-June compared to late-April, marking the largest increase since 2018. In terms of absolute freight rate change, it rose by USD 3651 per 40ft container, just above the USD 3566 increase during the pandemic in 2021.

Shippers with fear of a capacity crunch and further rate increases in ocean freight shipping later this year will continue to frontload their cargo.

This increasing demand could compound the current disruption and operational inefficiencies and eventually push further upward pressure on both ocean and air freight rates.

Therefore, shippers should monitor how the ocean container market evolves during its summer peak season when navigating their paths in the air cargo market.

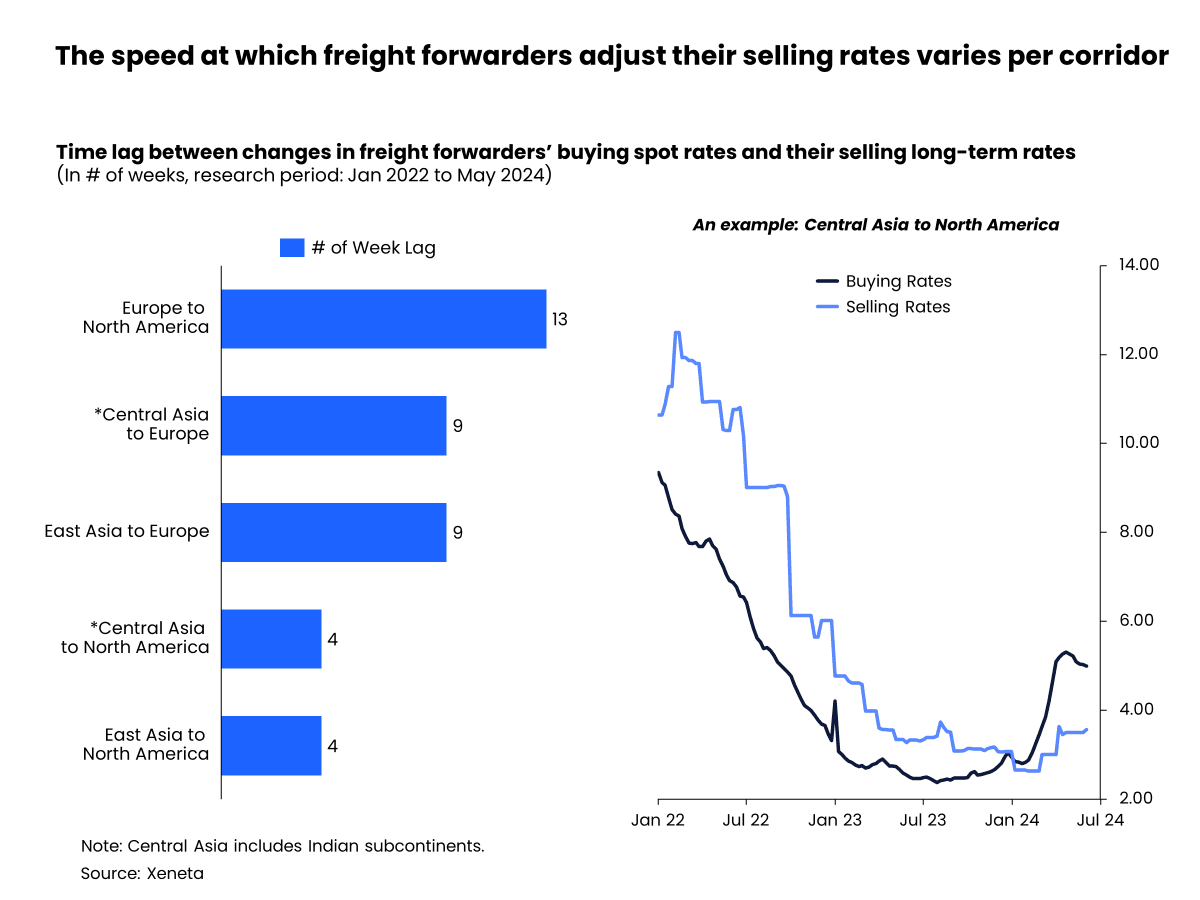

Timing the response window of shipper rates to airline rate adjustments

To understand the direction of the air cargo market, it is necessary to understand how quickly shipper contract rates respond to changes in airline spot rates.

To address this, Xeneta has analyzed the correlation between freight forwarders’ buying spot rates and their selling long-term rates on major fronthaul corridors.

Between January 2022 and May 2024, freight forwarders in the Europe to North America market tend to pass on changes in their buying spot rates to shippers within 13 weeks.

For Asia to Europe, shippers can expect rate adjustments in nine weeks. On the Asia to North America market, the response time is even shorter, taking just four weeks.

The differences in the response window may well reflect supply and demand dynamics, the absolute levels of buying rate changes, and freight forwarders’ procurement strategies across different corridors.

As demand growth has outpaced supply growth since the start of 2024, Xeneta has observed freight forwarders are now passing on freight rate adjustments more promptly. For instance, in the South Asia to Europe market, the response window for selling rates to their buying rates adjustments has been reduced from nine weeks to three weeks. As market demand surges, freight forwarders gain more negotiating power.

Shipper contract strategies

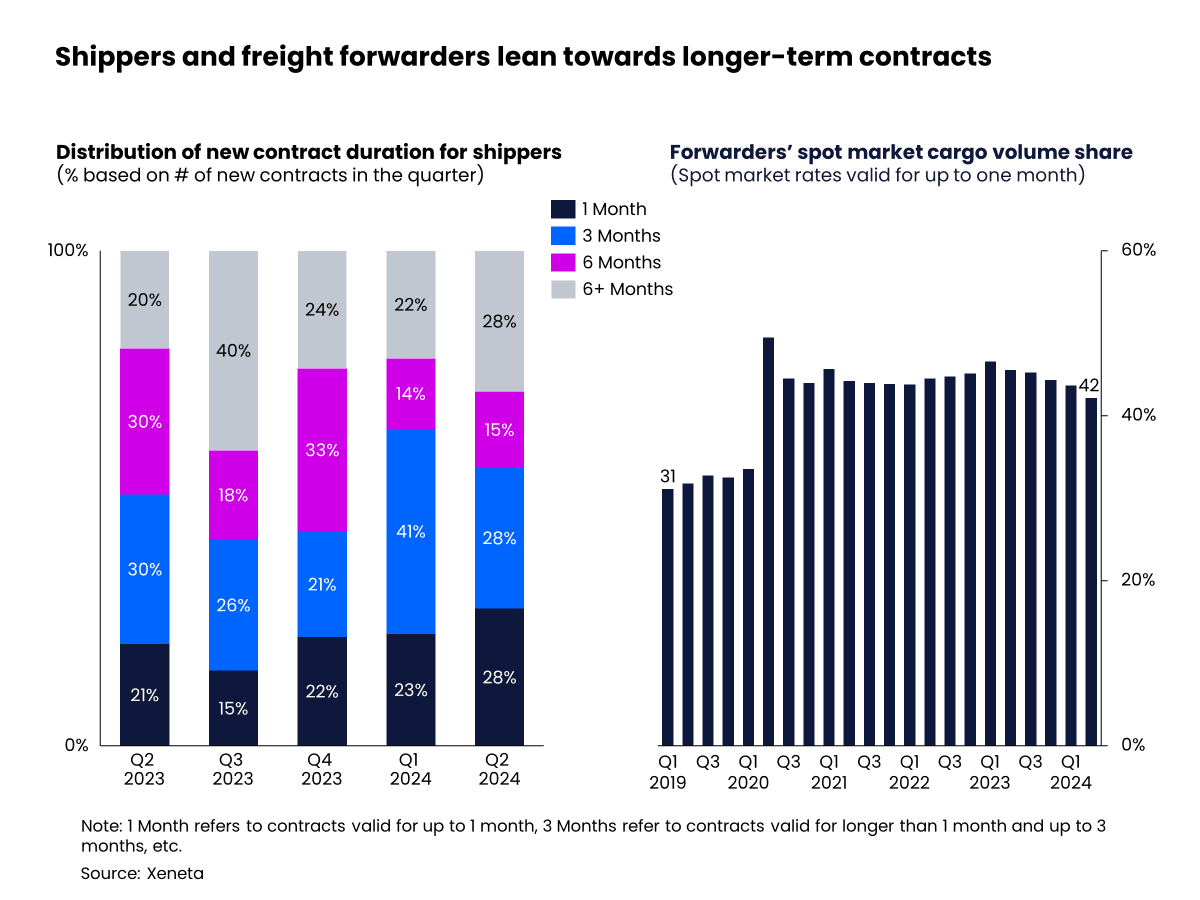

Given the rapid response to market fluctuations and the potential for a continued air cargo boom in Q4, shippers are once again adjusting their preferred contract lengths.

In the second quarter of 2024, contracts lasting more than six months topped the list, with an increasing share of 28%.

Shippers are shifting towards contracts longer than six months to avoid extreme freight rate fluctuations during the upcoming year-end peak season.

Equally popular are the three-month and one-month contracts, each holding 28% of the market share.

The decrease in three-month contracts suggests unease about renegotiating contracts just before the year-end peak season.

Conversely, the growing proportion of one-month contracts indicates shippers are facing increased pressure to hold on to longer-term contracts in the face of market volatility.

This is in line with the shorter freight rate adjustment window discussed earlier.

Given the many uncertainties in the market, it's becoming more difficult for shippers to agree on the best procurement strategy.

Fortunately for shippers, freight forwarders appear to share the same view, also procuring fewer cargo volumes in the spot market.

In the second quarter of 2024, the proportion of cargo volumes procured in the spot market accounts for 42% of the total market, showing a three-percentage-point decrease from a year ago, but still 10 percentage points higher than the same period in 2019.

As the market heads into the second half of the year, it may be ‘now or never’ to consider longer-term contracts.

With a mix of ocean shipping chaos, increased manufacturing activities, a fear-of-missing-out sentiment and soft consumer demand a delicate balance of short and long-term contracts is at the forefront of the minds of procurement professionals across the sector.

Only time will tell if the right bet is placed.