MACROECONOMICS

Air Freight

Quarterly overview of the majordevelopments on the macroeconomic landscape

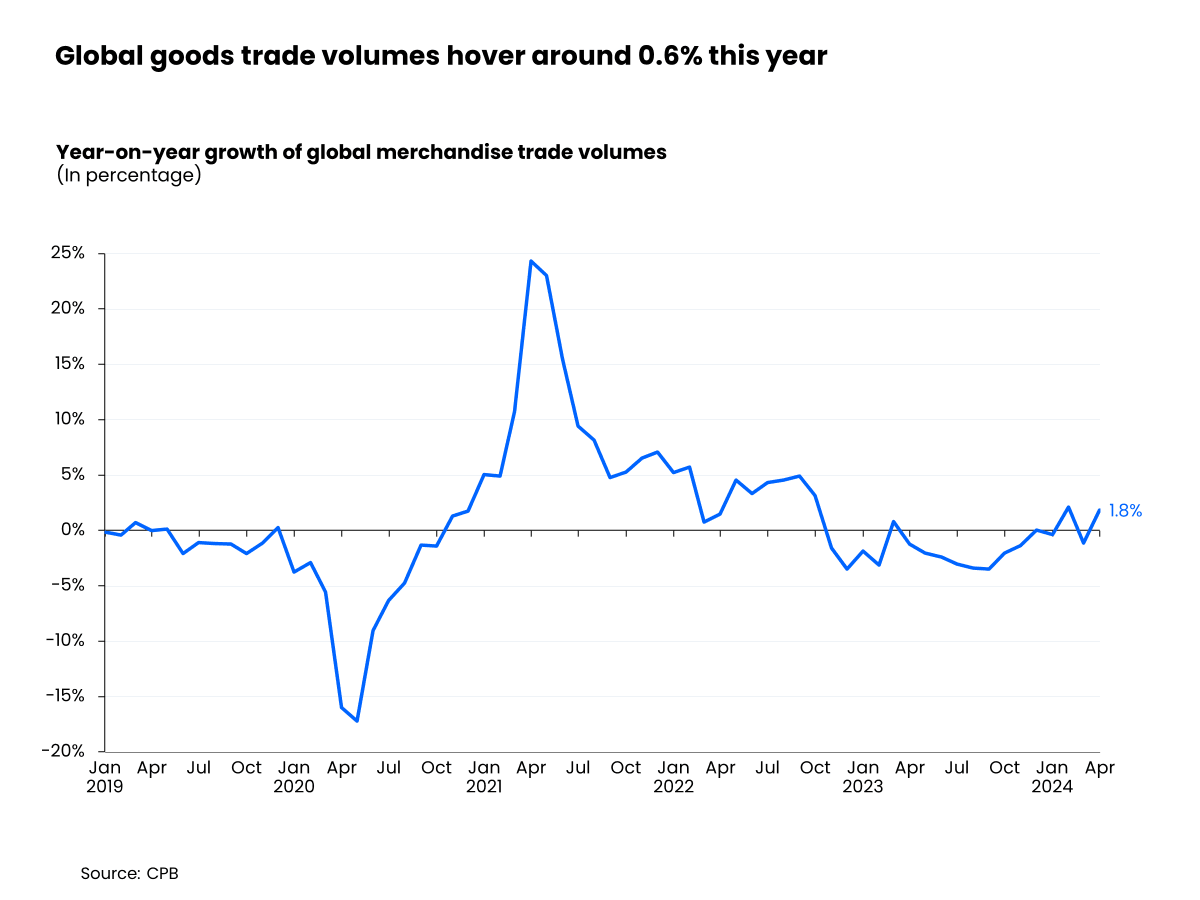

“Steady but slow” recovery of global trade

Macroeconomics provides the backdrop to the air cargo market and a consensus among the OECD, IMF and WTO is for growth in global trade to more than double in 2024, with further expansion in 2025.

Focusing on merchandise trade specifically, WTO’s latest outlook from April suggests world goods trade volumes will increase 2.6% in 2024 and 3.3% in 2025. This follows a 1.2% decline in 2023, due in part to high inflation.

The 2024-2025 outlook for global trade aligns broadly with expectations for global economic growth. This follows a relative shortfall in global trade relative to GDP growth in 2023. The IMF predicts world GPD growth will remain ‘steady but slow’ at 3.2% in 2024 and 2025, which is the same rate as 2023.

World merchandise trade volumes have reported around 0.6% year-on-year growth on average for two out of the first four months of 2024, according to the CPB.

US, EU and UK retail sales volumes, a key indicator of consumer confidence and demand, all reflect this trend.

These figures have hovered around 0% growth in the first five months of this year, suggesting a somewhat subdued outlook. But on a positive note, the overstocking issue from 2023 has been addressed.

Therefore, the recent surges in ocean and air shipping volumes are likely not due to increased consumer demand, but are a result of shippers front loading goods to avoid further disruptions from the Red Sea conflict, new tariffs on Chinese imports in the EU and US, and the possibility of a Trump presidency - which could see the imposition of 60% tariffs.

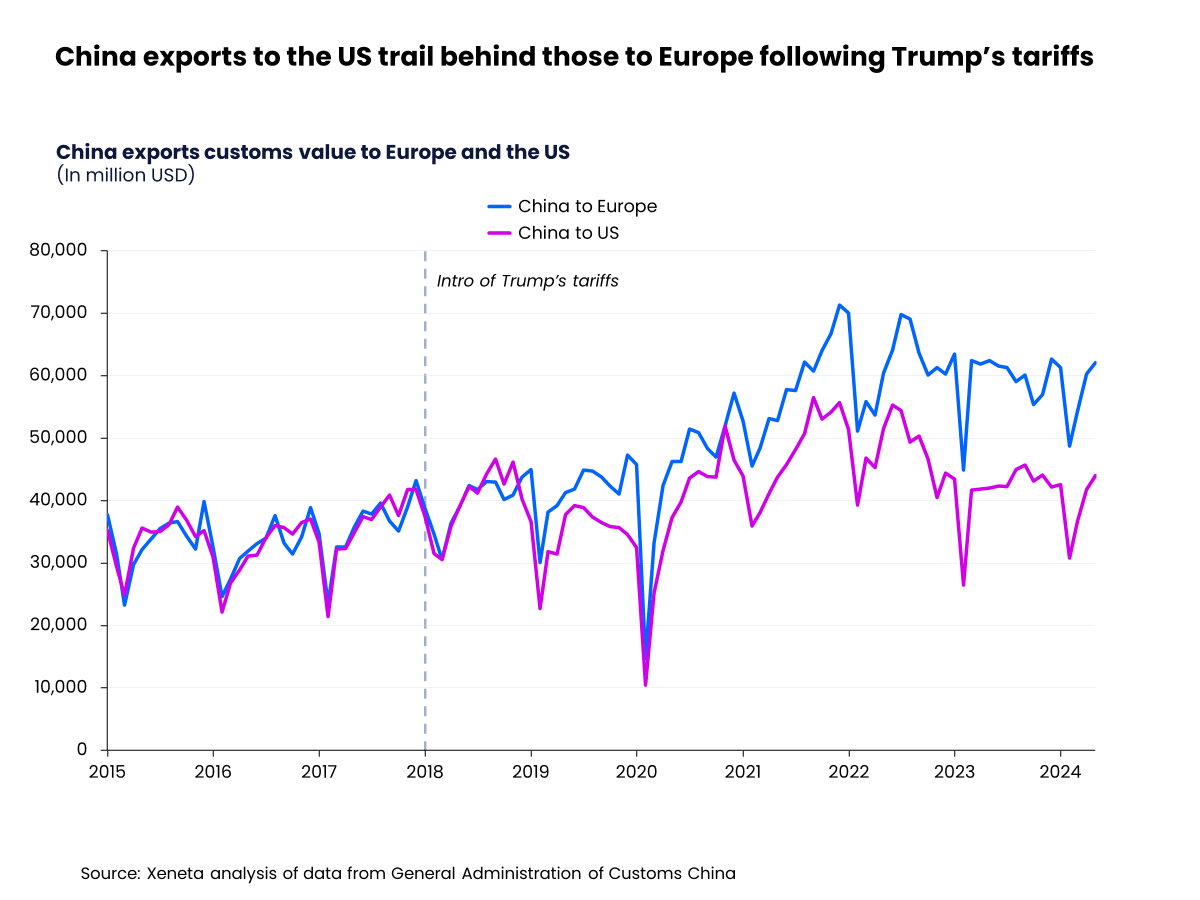

Impact of protectionism on trade patterns

The presence of increasing tariffs raises the question: Do they really work?

Looking back at history, in 2015, China's export volume and growth rate to the US was at a similar level to its exports to Europe. This trend continued until 2017, just before the US-China trade war.

With the introduction of Trump's tariffs on Chinese goods in 2018, China’s exports to the US only grew by 27% in the first four months of 2024 compared to the same period in 2017. In contrast, China’s exports to Europe, which were valued similarly to US exports in 2017, increased by 82% in the same timeframe.

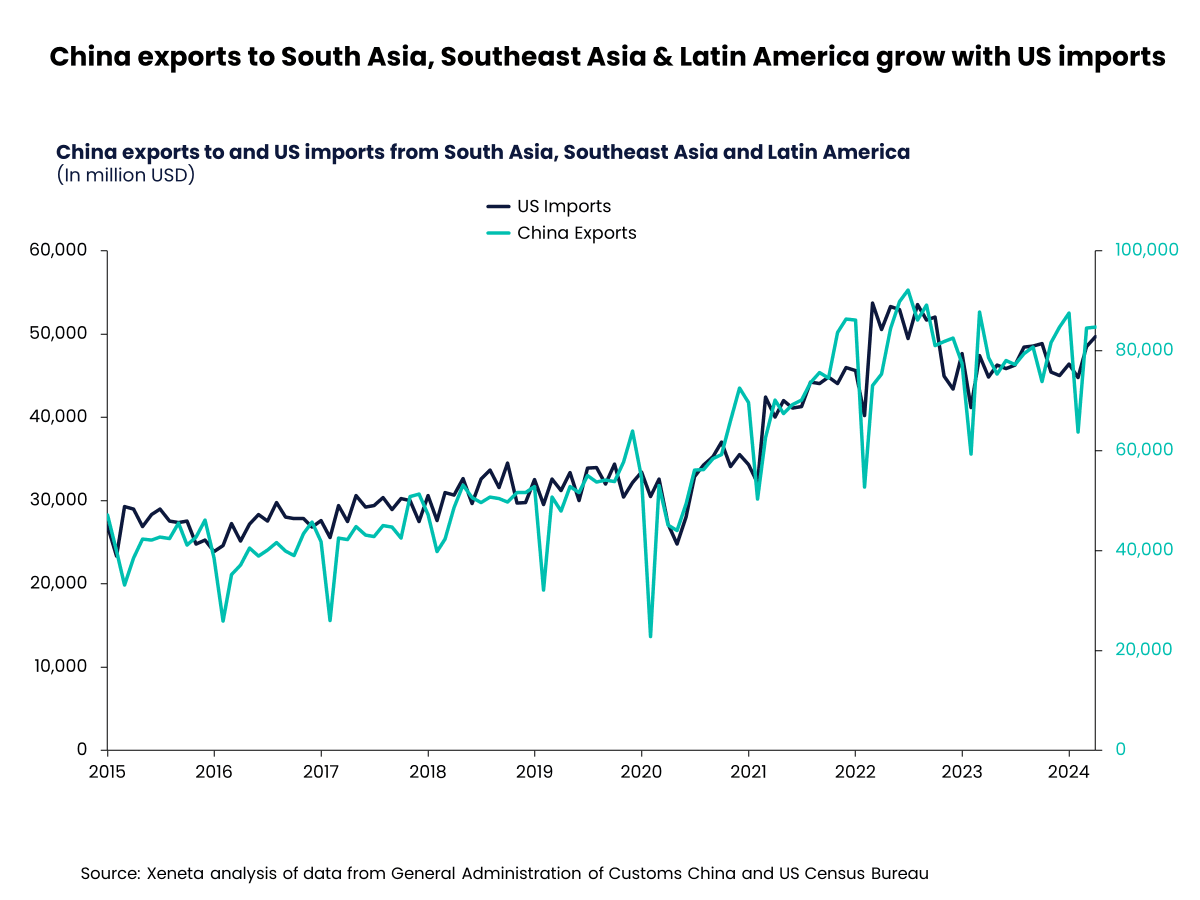

Increased protectionist policies and concerns about supply-chain resilience have seen some companies shift their supply chain sources to South Asia, Southeast Asia and Latin America.

As a result, US imports from these regions showed a 72% increase during the same period (source: US Census Bureau).

It is intriguing to note that China’s exports to these regions also surged by 110% during this period.

Observing the patterns of China exports and the US imports to and from these regions, it is evident that China exports have been growing in sync with US imports in recent years.

While protectionist policies may have impacted direct US-China imports/exports, trade found its way and flowed through other channels.

Therefore, if the US and EU introduce new tariffs, trade between China and South Asia, Southeast Asia and Latin America will likely expand further. As the IMF succinctly summarized, trade patterns are shifting.