Q2 2023

DEMAND

Quarterly overview of the majordevelopments in demand

Global air cargo demand was hit hard by the pandemic, with volumes still down 9% in June from 2019 levels. General cargo is the main laggard, with volumes down a considerable 15% on pre-pandemic levels.

However, there are some signs showing that the deterioration in global chargeable weight is easing, with volume down 3% year on year in Q2. The decline mostly come in April but slowed to -1% year on year in May and June.

This can be attributed mainly to easing contraction in global general cargo growth, with volumes dipping just 1% in Q2 from a year ago, 4 percentage points less than the Q3 level last year and the largest year-in-year decline since 2022.

In contrast, special cargo volumes registered their first decline (-1%) in Q2, with volumes having remained in positive territory during most of the pandemic on the back of the surge in pharma demand.

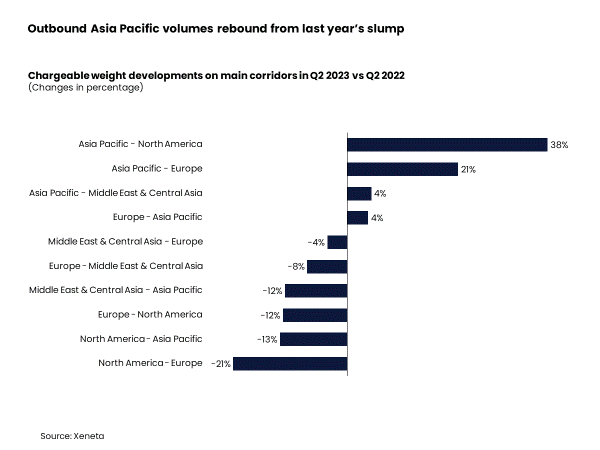

Turning to regional matters, the biggest Q2 winner was the outbound Asia Pacific, mainly due to the rebound of the Northeast Asia market following last year’s severe lockdown, especially in China. Chargeable weight from Northeast Asia to both North America and Europe soared 38% and 21%, respectively.

In contrast, the transatlantic market was the biggest loser in Q2, with chargeable weight declining by 12% year-on-year for westbound trade and 21% year-on-year for eastbound trade.

It is noteworthy, however, that in comparison to outbound Asia Pacific trades, the Europe to North America corridor was the best performer in Q2 last year, with volumes up 20% year-on-year to record levels versus 2021. So, the decline this year was mostly off exceptionally high volumes last year.

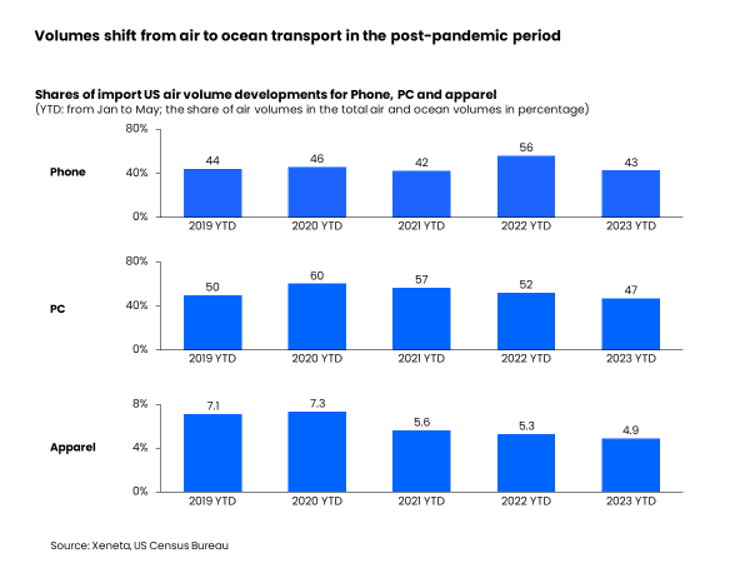

One other contributor to the current decline in global chargeable weight is modal competition with ocean shipping. Since mid-2022, improved schedule reliability of ocean transport has led to a reverse in the ocean-to-air shift that occurred during the pandemic. For example, on the Asia to North America West Coast trade, ocean schedule reliability reached 53% in May, up 31 percentage points from a year ago.

Evidence for this modal shift can be found in phone transport on the transpacific eastbound lane. According to the US Census Bureau, the volume share of phones using air freight was 44% in the first five months of 2019, rising to 56% in the same period of 2022.

In other words, the market share of containerized shipping shrunk by a considerable 12 percentage points versus air freight. As the disturbance in ocean shipping gradually eases, the phone market saw its air freight share in the first five months of this year fall back to only 43%, similar to the situation in 2019.

On top of this reverse shift, some shippers, and especially those with matured products (e.g., automotive shipments and machinery), are now evaluating whether to move volumes from air to ocean for the first time. Environmental concerns as well as cost optimization are likely to be the key drivers of this development.

This trend can also be observed in both the PC and apparel markets. The US Census Bureau shows that since it peaked at 60% of market share in the first five months of 2020, the air freight volume share of PC shipments fell to only 47% in the same period of 2023, down 3 percentage points from the 2019 level. Similarly, for the apparel industry, although largely taken by ocean shipping, the volume share using air freight was still down from 7.1% in the first five months of 2019 to only 4.9% in the same period this year.