DEMAND

Air Freight

Quarterly overview of the majordevelopments in demand

The main contributor to freight rate spikes in the 2023 year-end peak season was the recovery of demand.

In Q4 global air cargo demand grew by an average of 6% year-on-year, accelerating from 3% in October to 6% in November and 8% in December.

In terms of seasonal developments, global air cargo demand in Q4 increased by 7% quarter-on-quarter.

This was the third consecutive quarter of growth, albeit starting from a low base in Q1 2023, which saw the lowest demand since Q3 2020.

The 7% growth was more notable in comparison to Q4 2022, which was mostly flat and only up a meagre 2% quarter-on-quarter.

Among the world’s top corridors, the Asia Pacific to North America and Europe markets saw double-digit quarterly demand growth of 11-12% in Q4.

Following closely was the Europe to Middle East market, which recorded an 8% demand growth in the same quarter.

The demand growth from Europe to North America was in line with the average global air cargo demand growth (+7% quarter-on-quarter).

A surge of e-commerce volumes

In Q4, a surge of e-commerce demand, which it is claimed occupied most of capacity out of China, was a frequent topic of conversation with industry stakeholders and widely reported in the news.

But was this really the case? The answer may be found in statistics reported by the US.

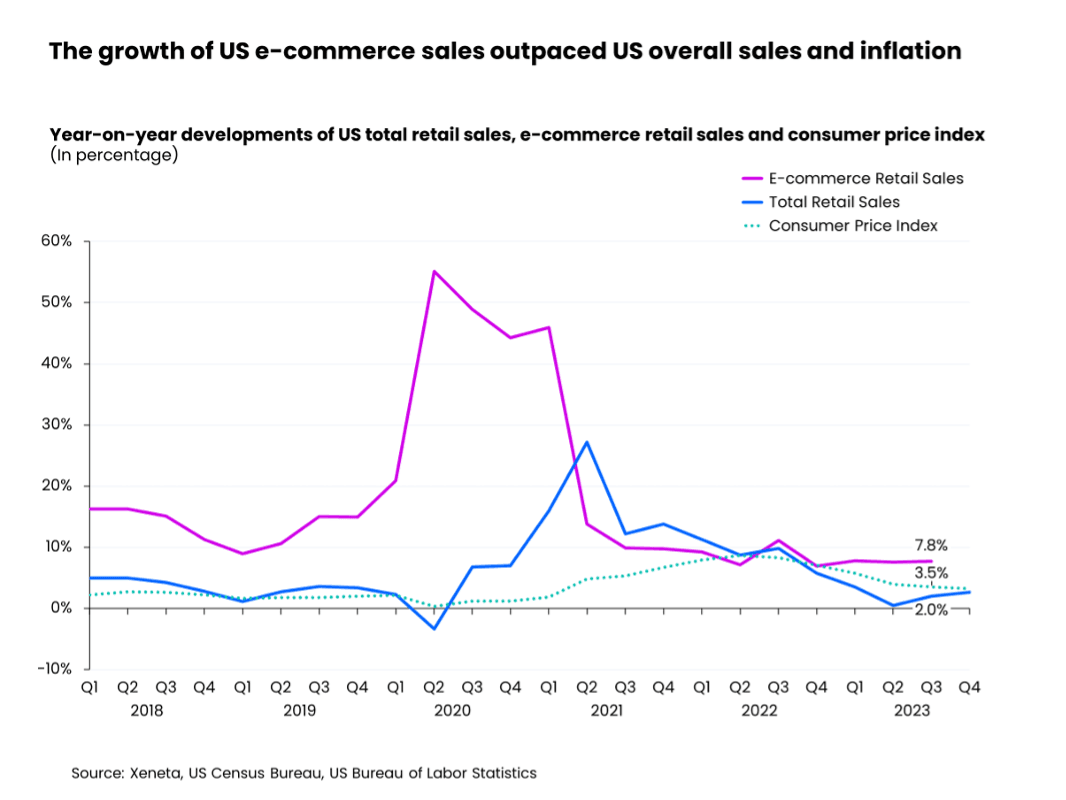

In the US, e-commerce sales accounted for 15% of total retail sales in Q3 2023. And the year-on-year growths in US e-commerce sales have been surpassing the growth of US total retail sales for most of the past six years (source: US Census Bureau). The only exception was between Q3 2021 and Q2 2022, when overall retail sales experienced a significant boost due to pandemic-related shopping sprees.

Then came soaring inflation…

Although both US e-commerce retail sales and total retail sales continued to grow on average by 8.5% and 8.8% year-on-year respectively in 2022, a large portion of this growth was offset by an annual inflation rate of 8.0% in the same year (source: US Bureau of Labor Statistics).

In Q1 2023, the growth of US e-commerce retail sales rebounded from the trough seen in Q4 2022 (+6.9% year-over-year). By Q3 2023, e-commerce sales had risen 7.8% year-on-year. This suggests positive growth in e-commerce volumes against the backdrop of a slowdown in annual inflation to 3.5% year-on-year in the same period. In contrast, Q3 US total retail sales grew only 2.0% year-on-year at a slower pace than the annual inflation.

Further evidence can be found in the monthly advance reports on US retail sales from non-store retailers, which shows nearly 70% of sales have come from e-commerce.

These non-store sales account for around 60% of total e-commerce retail sales in the US.

The latest statistics from the US Census Bureau show sales from non-store retailers grew at accelerated rates in 2023, from 6.5% year-on-year in September to 9.0% in October and further to 9.5% in November.

Only in December did it experience a dip to 7.0% year-on-year. Once again, this indicates a surge in e-commerce demand during the year-end peak cargo season.

Looking ahead, we anticipate e-commerce sales will continue to outpace the growth of total retail sales in 2024, with an increase in e-commerce volumes.

This will contribute to the growth of overall global air cargo demand in 2024, which Xeneta expects 1-2% year-on-year.

Shift from ocean to air transport is brewing once again

In late November 2023, air freight transport was 23 times more expensive than ocean freight, reaching its highest ratio since 2021.

In addition to the increase in air cargo demand during the year-end holidays, the air to ocean ratio hike in late November was a result of improved schedule reliability as ocean container shipping recovered from the pandemic chaos. It was also due to a flood of new capacity entering the market, which pulled ocean freight rates down.

However, recent disruptions in ocean shipping due to the Red Sea crisis have led to substantial surcharges being added to rates and approximately an additional 10-day increase in one-way transit time for ships avoiding the Suez Canal.

By the week ending 14 January, the air cargo spot rate was only six times higher than the ocean spot rate, a significant decrease from the previous month and also below its pre-pandemic 2019 average level of nine times more expensive.

As the Lunar New Year approaches on 10 February in China, South Korea, and Vietnam, a surge in shipments before the holiday are expected. This, combined with the current strain on ocean shipping, increases the likelihood of a shift from ocean to air transport or sea-air transport for time-sensitive high-value cargo and subsequent increases in air freight rates. (More details can be found in this week’s air blog.)