SUPPLY

Air Freight

Quarterly overview of the majordevelopments in air freight supply

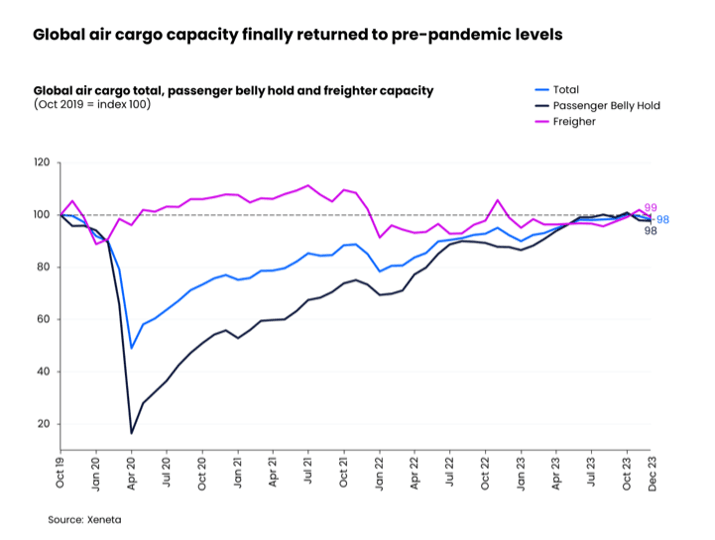

In October, global air cargo supply finally returned to its pre-pandemic level, when compared to the same month in 2019, thanks to continued recovery of belly capacity due to increasing passenger travels.

However, as carriers transitioned to winter season schedules, which are valid from the end of October to the end of March 2024, the market experienced a 3% decrease in global belly capacity in the November-December period compared to October.

In response, ‘traditional’ seasonal increases of capacity were observed. In November, the market saw a 3% month-on-month increase in global capacity to cover the missing belly capacity and meet rising demand during the year-end. By late December, this fell back to its October level as the surge of cargo demand eased.

Driven by cargo demand, dynamic load factors for major fronthaul routes increased in December.

This is in stark contrast to December 2022, when dynamic load factors on all major fronthaul routes fell sharply by 9-12 percentage points.

In December 2023, the Asia Pacific to North America corridor registered the highest dynamic load factor among global top corridors.

Despite continued recovery of capacity, the load factor edged up by 1.3 percentage points from December 2022 reaching 86%.

This was seen on the China to US market due to limited belly capacity and a surge of e-commerce demand.

This saw the load factor on this route reach 95% in December 2023, which was an increase of four percentage points compared to the previous year.

The next highest dynamic load factor is found on the Asia Pacific to Europe corridor which stood at 83% in December, a five-percentage-point year-on-year increase. The China westbound market had a load factor of 88% which, similarly to the Transpacific market, is above the market average of 59% and indicates constraints in available capacity due to increasing demand.

The load factor on the Europe to North America market took the third place with 75%, but this was more a result of capacity reductions during carriers’ winter season. In December, the capacity on this market decreased by 19% from its October level prior to the scheduled capacity cuts.

When looking at backhaul trades, it is not surprising to see the return legs of the above-mentioned top three trades experienced significant load factor declines year-on- year.

In December, the cargo holds on these return-leg flights were half empty.

In light of this, it remained challenging for all-cargo carriers to maintain profitable rotations in Q4.

For example, Flexport struggled to operate profitable freighters and was reported recently to have been filling empty space on its on-lease freighters on return legs through interline partnerships with Westjet (source: Loadstar).

Although available global air cargo capacity in Q4 increased to pre-pandemic level, the market continued to be exposed to disruptions caused by ongoing staff shortages and extreme weather conditions.

Strikes at the DHL Express CVG Hub, high staff illness at Cathay Pacific and Lufthansa, as well as extreme winter conditions at Frankfurt, Germany and Anchorage have disrupted airline schedules and available cargo capacity during the year-end peak season. This was, to some extent, responsible for the year-end rate spikes in 2023.

Furthermore, the grounding of the Boeing 737 Max due to flight safety issues has added strain to the market. However, due to its narrow-body design, the impact will be limited to the regional rather than long-haul cargo market.

Looking ahead, all eyes are on capacity recovery on the Northeast Asia market, especially China. By the end of 2023, China's international passenger flights had recovered to 63% of pre-pandemic levels (source: Jiemian).

The Civil Aviation Administration of China has set a goal to restore more than 90% of the total number of flights in 2019 by the end of 2024.

However, many uncertainties remain. For example, geopolitical tensions and the impacts of the Russia-Ukraine war continue to hinder the recovery of China-US passenger flights.

Starting in November 2023, China and US aviation authorities planned to increase weekly direct flights from 48 to 70, but this still represents less than 20% of pre-pandemic levels.