RATES

Air Freight

Quarterly overview of the majordevelopments in air freight rates

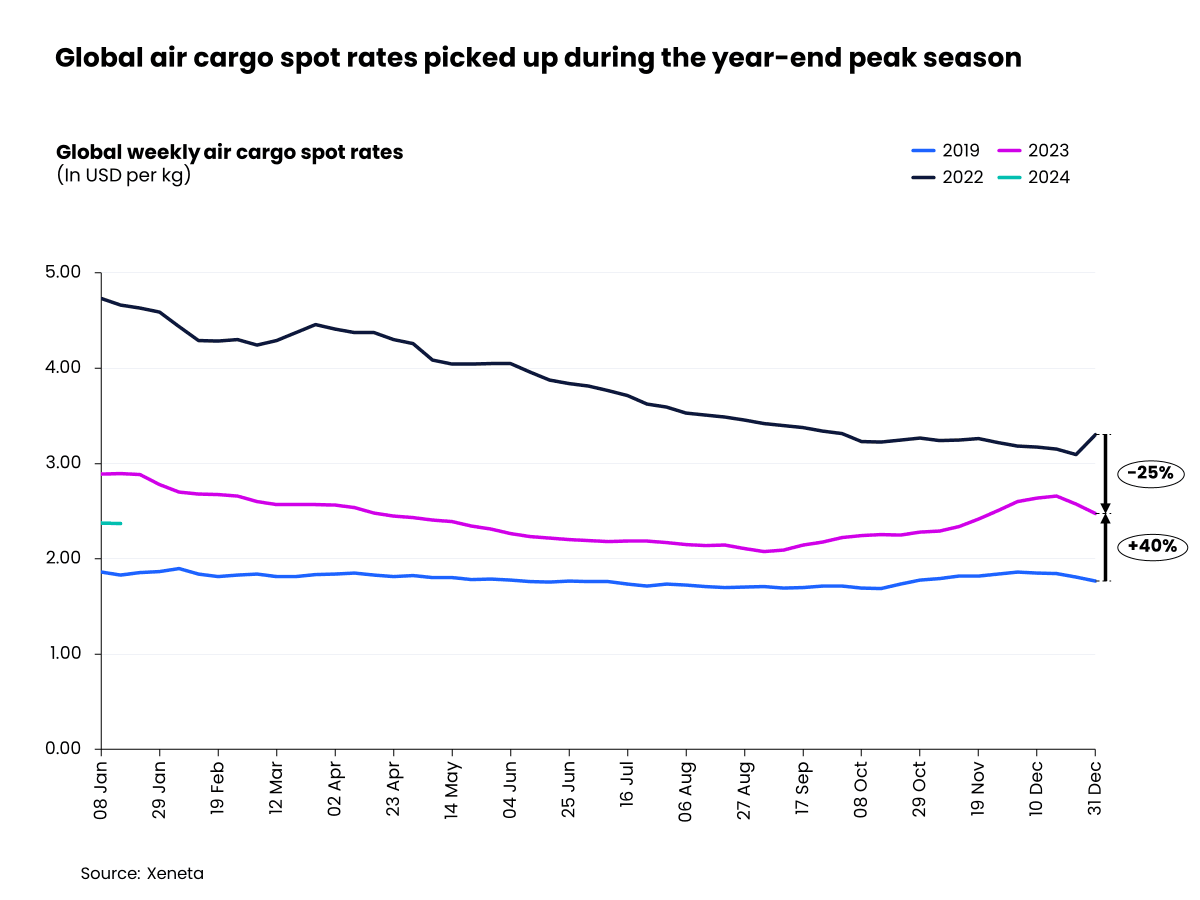

Global air cargo spot rates edged up in Q4 2023, surging by 21% in December compared to the August low to stand at USD 2.59 per kg. This can be mainly attributed to increases in air cargo demand triggered by e-commerce out of Asia. It is in contrast to the peak season in 2022 which saw a stagnated market.

But this surge in demand was not enough to reverse the year-on-year decline in spot rates witnessed throughout 2023. Spot rates in the last week of December 2023 were 25% below the rates recorded in the final week of 2022. However, the average global spot rate recorded at the end of December 2023 was still 40% above its pre-pandemic level in the corresponding period in 2019.

The global average general cargo spot rate has been falling below its seasonal rate since June 2022 due to weakened demand. However, there was a narrowing in the price gap between the two in Q4 2023.

By mid-December the price difference between the general cargo spot and seasonal rates shrunk to just two cents after global air cargo demand spiked in the two weeks prior.

However, as the holiday season came to an end, general air cargo spot rates saw a notable decline, falling to USD 2.11 per kg in the week ending 14 January. This is a 12% decrease from its peak four weeks prior.

In contrast, general cargo seasonal rates remained relatively stable during this period, reaching USD 2.42 per kg in the week ending 14 January.

The spikes in air cargo rates boosted carriers' Q4 2023 cargo revenues, growing 15% quarter on quarter. This marks the first quarter-on-quarter increase since Q2 2022.

In terms of year-on-year comparison, Q4 2023 cargo revenues registered a further downward trajectory, falling by 19% compared to the same quarter in 2022. This is the sixth successive quarterly decline.

It is worth noting that Q4 2023 global carrier revenues continued to outperform their Q4 2019 level by 25%, thanks to rising jet fuel surcharges and compensation for other operating costs.

In Q4, the average US Gulf Coast Kerosene-Type jet fuel spot prices declined by 18% compared to Q4 2022 but remained 43% higher than Q4 2019.

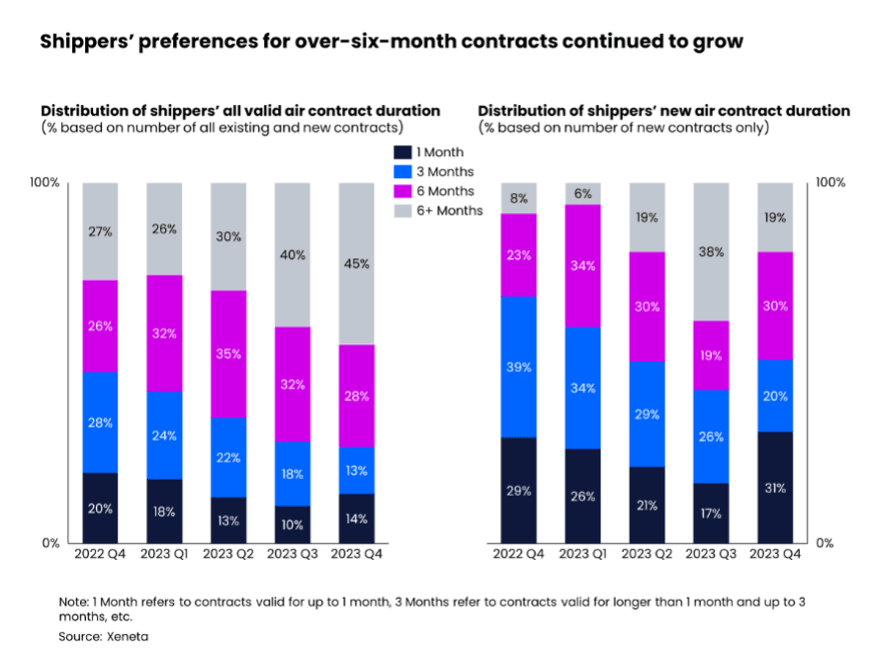

As the global air cargo rates continued to fall from the heights of the pandemic, more shippers returned to longer-term contracts.

The share of all shipper contracts valid for more than six months grew for a third consecutive quarter in Q4 2023, accounting for 45% of all valid contracts and a five-percentage-point increase compared to Q3.

With the potential for a more stable market on the horizon, shippers have also been contracted with fewer logistics service providers. At its most extreme during the pandemic, some shippers were managing a portfolio of 11 service providers due to the severe capacity squeeze, but this number halved in Q4 2023.

In Q4 2023, freight forwarders continued to procure around 44% of global volumes from carriers on the spot market. However, looking more closely within Q4 data, the spot market share fell to 42% in December, which is a three percentage-point decrease from its October level.

Freight forwarders’ spot market share in Q4 2023 remained higher than pre-pandemic when it accounted for only one third of total market volumes.

With freight forwarders around the world exposed to recent spot rate surges, Xeneta has observed an increase in rates on newly-signed longer-term contracts with shippers. For instance, on China to the US corridor, long-term rates on recently signed contracts increased by 18% in December from September levels.

This is also reflected in shippers’ preferred contract duration. Agreements signed in Q4 2023 lasting more than six months accounted for just 19% of total new contracts, down 18 percentage points from the previous quarter. Meanwhile, the share of new contracts valid for up to one month increased to 31%, up 14 percentage points from the previous quarter.

This presents a tricky situation for upcoming contract renewals, with shippers likely to find themselves exposed to hefty premium rates. In addition to the impact of the year-end seasonal spike, shippers should also brace for potential spillover from the chaos caused in ocean freight by the Red Sea crisis.