Ocean Market News By Xeneta

May 9, 2024

Market News by Xeneta May 9, 2024

Visit Xeneta Customer Portal

(IQ Hub) For

Exclusive Market Content

The Xeneta Ocean iXRT provides an overview of market movements, the key risks and issues to be aware of and insight on how these may develop in the coming weeks and months. Xeneta also publishes an iXRT report dedicated to the air freight shipping market, with the latest edition available here.

Topics covered in this edition of the iXRT Ocean include:

Long term rates slightly up in May.

Shippers securing lower long term rates than freight forwarders.

Maersk Ocean posts losses in Q1.

Schedule reliability remains in the doldrums.

Congestion increasing in several major ports.

Carriers’ demand for capacity remains high.

2030 plans revealing ambitious fleet growth targets.

OCEAN RECAP

For many shippers May brings the start of new one year contracts, especially on trades into the US.

The good news for those shippers is that, while the spot market remains considerably above last year’s levels, this has not translated into a similar increase for long term rates.

These new long term rates are however slightly higher than the market average in April.

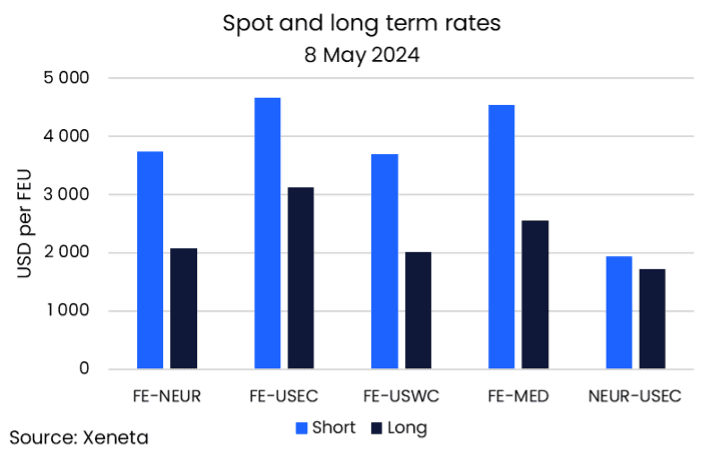

For example, from the Far East to the US West Coast the average long term rate for contracts entering validity within the past three months rose from USD 1 880 per FEU at the end of April to USD 2 010 per FEU on 8 May.

While this represents an increase in long term rates, it is still 46% lower than the average spot rate on this trade, which also rose from the end of April to reach USD 3 696 per FEU on 8 May.

An even smaller increase was registered in long term rates from the Far East to the US East Coast.

These rose to USD 3 120 per FEU on 8 May, which is just 1.6% higher than on 30 April.

Here too the spot market is considerably higher, averaging USD 4 660 per FEU, having increased by almost USD 500 per FEU from the end of April.

Taking a slightly longer view of market movements and average long term rates from the Far East into the US are also higher when compared to 12 months ago.

Into the US West Coast long term rates are up by 10% year over year while rates into the US East Coast have increased by 2%.

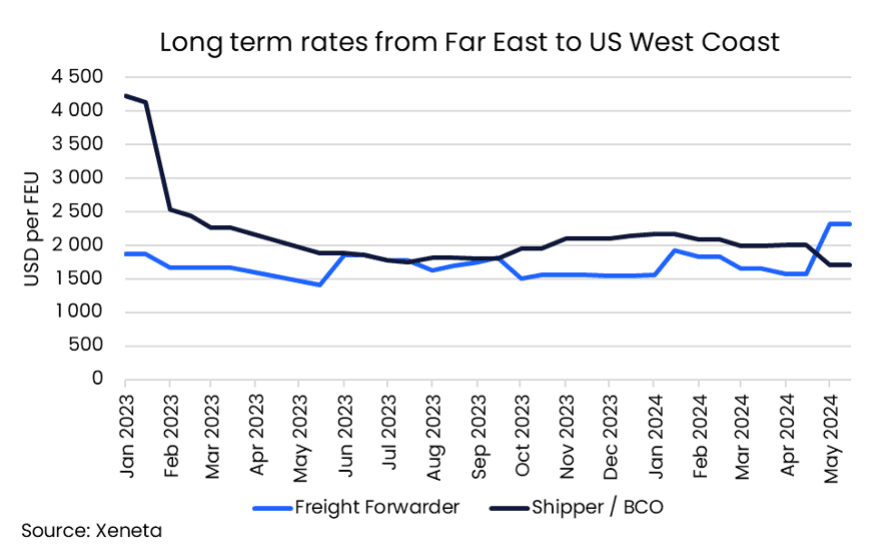

Diving deeper into this data reveals a split in the market between the rates secured by shippers and freight forwarders.

For example, looking at the average long term rates of contracts entering validity in the past three months, freight forwarders are now seeing rates around USD 350 per FEU (40ft equivalent shipping container) higher than shippers from the Far East into US West Coast and USD 400 per FEU higher into the US East Coast.

While shippers have been able to secure rates below the market average, and importantly below what they got at this time last year, freight forwarders have seen a jump in rates.

This is a reversal of the market dynamics seen during the past year when freight forwarders were typically able to secure slightly lower rates.

Maersk Ocean losing money despite higher rates

Despite the higher rates resulting from conflict in the Red Sea, Maersk’s latest financial results reveal the carrier’s ocean business recorded a loss in Q1 for the third consecutive quarter.

While the latest loss of USD 161 million (EBIT) is an improvement from Q4 2023 when it lost USD 920 million, it is still an underwhelming financial performance given the significant shift in market conditions.

Maersk’s volumes increased by 7.5% from Q1 2023 moving 2.9m FFE (40’ equivalent), slightly lower than global growth in container volumes over the same period.

Compared to Q4 2023, Maersk’s average freight rate (adjusted for volumes) was up by 23.0%, but at USD 2 368 per FEU, it is still down by 17.5% compared to Q1 2023.

The drop in average rate can largely be explained by Maersk’s high exposure to the long term market, with 75% of its Q1 2024 volumes moved on a contracted basis.

This is expected to fall to 70% for the full year 2024.

That the long term market has not been driven up to the same extent as the short term market following the escalation of conflict in the Red Sea is demonstrated by the Xeneta Shipping Index.

The XSI®, which is a global measure of all long term contracts in the market, was in fact slightly lower at the end of Q1 2024 than at the end of Q4 2023.

OCEAN OBSERVATION

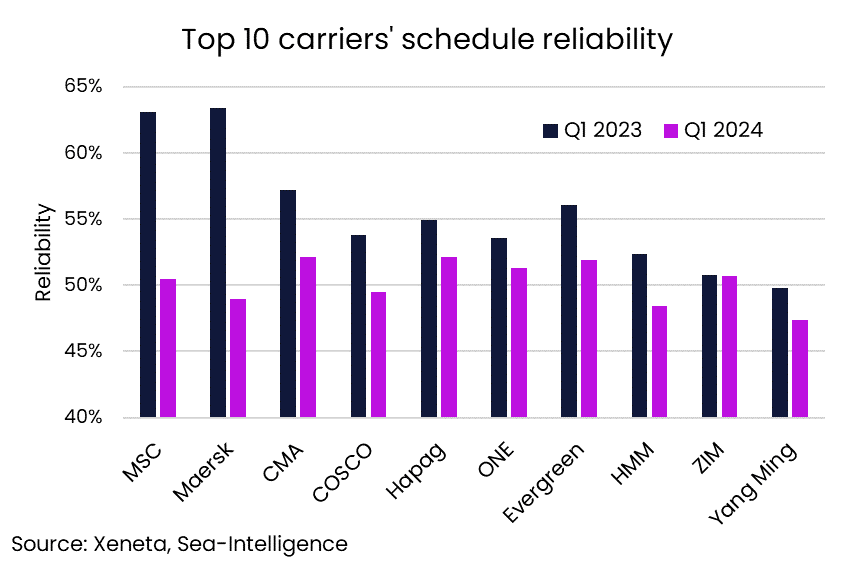

Carriers continue to struggle with schedule reliability, with Q1 results showing that no carrier had more than 55% of its ships arriving on time globally.

‘On time’ is defined as the ship reaching its destination within +/- one day of its scheduled arrival.

Out of the 10 biggest global carriers Hapag-Lloyd performed best in terms of schedule reliability, though there is little to celebrate with only 52% of its ships arriving on time in Q1.

Wan Hai, the world’s 11th largest carrier scored slightly better at 54%.

There was little difference between the schedule reliability of the top 10 global carriers, with the worst performing being only 4.7 percentage points lower than the best.

In Q1 Yang Ming had the lowest number of on time arrivals at just 47.4%.

While the conflict in the Red Sea has clearly had on impact on ships arriving at their destination on time, the fact that for several carriers there is relatively little change in performance compared to a year ago suggests schedule reliability has been a longer standing problem.

In Q1 2023 the best performing top 10 carrier was Maersk with a score of 63.4%, while Yang Ming (similarly to Q1 this year) was the worst performing at 49.8%.

Looking at schedule reliability at trade level shows that less than half of the ships sailing from the Far East to Europe and the US arrived on time in March.

The worst performing major trade in terms of schedule reliability was the Far East to North Europe where less than two out of every five ships arrived on time (37.2%).

This was followed closely by the Far East to US East Coast trade at 37.6%.

Both of these trades are impacted by the situation in the Red Sea and Suez Canal while the trade into the US East Coast is also hampered by restrictions in the Panama Canal.

However, even on the Transpacific trade into the US West Coast, which has a straightforward sailing route without any canal transits, only 49.3% of ships arrived on time.

Schedule reliability is likely to continue to be poor with port congestion becoming an increasing problem.

Carriers are reporting delays at major hubs in the Far East due to poor weather, while there are also higher waiting times in certain Mediterranean ports which are being used as transshipment hubs.

Ultra large container ships, having made the journey from the Far East around the Cape of Good Hope, unload their volumes at western Mediterranean ports which are then loaded on feeder vessels and transported onwards to central and eastern Mediterranean ports.

While this helps to ease the sailing distance of the ultra large ships, allowing them to make the return journey back to the Far East sooner, it is creating significant congestion at western Mediterranean ports.

One place where container congestion has not seen a significant increase is the US East Coast, despite the closure of the Port of Baltimore.

The reason for this lack of congestion is that ships bound for Baltimore already had scheduled stops at other ports on the US East Coast where containers could be offloaded with limited disruption.

OCEAN OUTLOOK

The latest volume data reveals March was another strong month of year-on-year volume growth for ocean freight container shipping globally, up by 5.1% compared to 12 months ago.

This means global demand in Q1 2024 was up by 9.2% from Q1 2023 and the highest growth since 2021.

Year-on-year growth in global reefer volumes is slightly lower at 7.7%, though this is largely due to reefer volumes not falling as low as dry containers in Q1 2023.

This growth in actual demand is compounded by diversions around the Cape of Good Hope, which the majority of the top 10 carriers are continuing to take.

The extra transport work caused by these longer sailing distances means more ships are required to maintain service schedules. New ships are therefore deployed straight onto these trades as soon as they are delivered and the idle fleet remains low.

Carriers are also keen to hang onto their ships, with only 20 scrapped in the first four months of the year. This means only 30 700 TEU of capacity has left the global fleet.

The largest ship scrapped so far this year being a 3 400 TEU 1993 built MSC vessel. Only one of the demolished ships was built in the 21st century.

While the Red Sea diversions mean carriers’ short term attention is on ensuring they have the ships to fill their scheduled sailings, in the longer term (and beyond the Red Sea crisis) overcapacity remains the looming concern

This overcapacity concern also explains the gap between the spot market and new long term freight rates.

With carriers fearing spot rates will fall if there is a large-scale return to the Red Sea, they may be sacrificing trying to push long term contract rates even higher in order to secure long term volume.

This outlook has also dampened carriers’ appetite for further additions to their orderbooks. So far this year 29 new ships have been ordered totaling 230 000 TEU, which is a 60% reduction from the first four months of 2023. The ships ordered so far this year are set to be delivered between the end of 2026 and into 2028.

A reduction in orders for new ships would make sense given the looming overcapacity concerns and uncertainty over new environmental regulations.

However, several carriers have recently announced 2030 plans, some of which have ambitious plans for fleet growth. Leading the pack are ONE and HMM who, alongside Yang Ming, will be left in a much smaller THE Alliance once Hapag-Lloyd leaves by the end of January 2025.

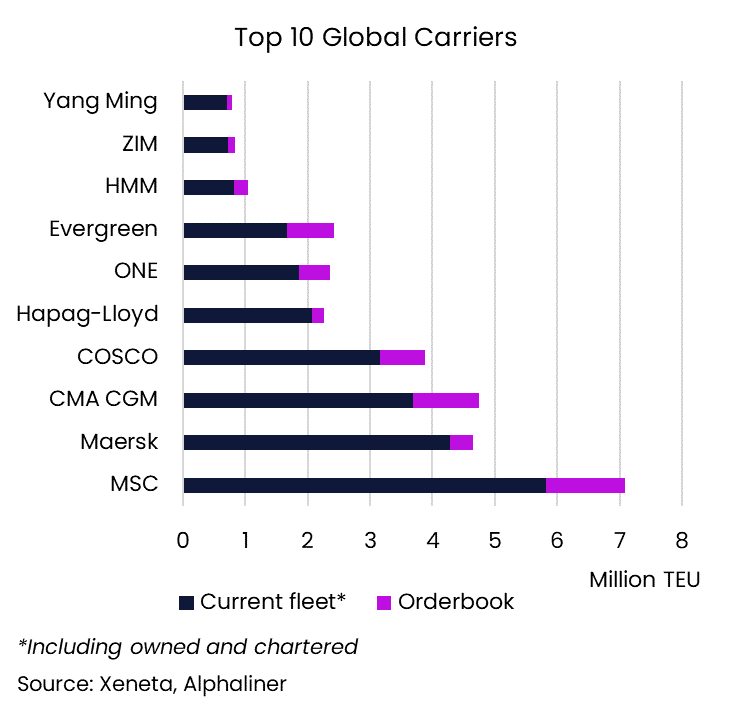

ONE leads the pack, with a target of increasing its fleet size to three million TEU by 2030.

ONE’s current fleet stands at 1.86m TEU, of which it owns 42% with the remainder chartered in. It’s current order book stands at 0.5m TEU (source: Alphaliner).

South Korean owned HMM has also set its sights on growth ahead of 2030, with an ambition of increasing its fleet from its current level of 0.82m TEU to 1.5m TEU by 2030.

The release of this target coincided with the announcement of USD 2.5 billion investment by the Korean state into its shipping industry, which includes fleet growth – a byproduct of which is more work for its shipbuilding industry.

Hapag-Lloyd has also released its 2030 plan and, while it has not been as specific as ONE and HMM on its fleet growth strategy, it has stated its ambition to consolidate its place among the top five container shipping carriers.

Investment in fleet will be required to achieve this ambition as, while Hapag-Lloyd may be the fifth largest carrier currently in terms of fleet size, when orderbooks are taken into account it drops to seventh behind ONE and Evergreen.

Also included in its 2030 plan is an ambition to reduce its greenhouse gas emissions by around one-third by 2030, on its way to net-zero fleet operations by 2045.

Having a larger fleet by no means guarantees greater market share and securing more volumes in a market dominated by overcapacity will come at a cost.

An example of this strategy is found in MSC which over the past few years has been aggressive in freight rates in order to fill up its fast growing fleet.

Betting on substantial growth in demand to keep fleet utilization up in an expanding fleet seems a risky move given the starting point is the current position of overcapacity in the market (albeit currently occupied due to the Red Sea situation).

Xeneta is the leading ocean and air freight rate benchmarking, market analytics platform and ocean container rate index, Xeneta Shipping Index (XSI®).

Xeneta’s powerful reporting and analytics platform and data density provide liner-shipping stakeholders the insights they need to understand current and historical market behavior – reporting live on market average and low/high movements for both short and long-term contracts.

Xeneta’s data is comprised of over +450 million contracted container rates and covers over 160,000 global trade routes. Xeneta is a privately held company with headquarters in Oslo, Norway and regional offices in New York and Hamburg. To learn more, please visit www.xeneta.com

NOTE: The XSI® public indices reports are based on long-term contracts only.

© 2024 Xeneta AS

Quarterly Market Average, 40' Container

Monthly Market Average, 40' Container

Quarterly Market Average, 40' Reefer HC