Ocean Market News By Xeneta

March 7, 2024

Market News by Xeneta March 7, 2024

Visit Xeneta Customer Portal

(IQ Hub) For

Exclusive Market Content

The Xeneta iXRT Ocean provides an overview of market movements, the key risks and issues to be aware of and insight on how these may develop in the coming weeks and months. This is the first dedicated Ocean edition of the iXRT report. The first edition dedicated to air will be published on 21 March.

Topics covered in this edition of the iXRT Ocean include:

Spot rates continue to soften on all trades out of the Far East into Europe and US.

Capacity deployed between Far East and Europe increases 19% year-on-year as services settle into Red Sea diversion.

MSC increases deployed capacity between Far East and Europe by 54%.

EU commission approves CMA CGM’s takeover of Bollore Logistics.

Lidl Tailwind expands into Hinterland logistics.

Shippers pushing hard to renegotiate rates and phase out Red Sea surcharges.

10 percentage point increase in shippers opting for three to six month contracts due to Red Sea risk.

OCEAN RECAP

March has brought a further drop in spot rates on the world’s biggest trades.

Xeneta data reveals spot rates from the Far East to the Mediterranean have fallen back below USD 5 000 per TEU, and rates to North Europe are back under USD 4 000.

Just as when spot rates were rising following the escalation of conflict in the Red Sea in mid-December, the market on trades from the Far East to the US have followed a similar pattern as those into Europe, only with a delay of around 15 days.

While rates into Europe peaked in mid-January and have since fallen by 19.5% (FE-MED) and 17.7% (FE-NEUR), rates into the US peaked around 15 days later at the start of February.

Since then, spot rates into the US West Coast have fallen by 10.3%, leaving them at USD 4 320 per FEU, and by 9.2% into the US East Coast, to stand at USD 5 680.

Though spot rates from North Europe to the US East Coast peaked around the same time as those from the Far East, the transatlantic trade has seen a slower pace of decline, down by 5.4% since early February.

Services settle into Red Sea diversion

Carriers have adjusted their fleet to the longer transit times around the Cape of Good Hope as part of diversions away from the Red Sea.

A recent Alphaliner report reveals overall capacity deployed between Asia and Europe is up 19% from a year ago.

This has been enough to keep average capacity leaving Asia for Europe so far this year in line with last year’s levels.

MSC’s increasing presence

Perhaps unsurprisingly given its aggressive fleet growth, MSC is the carrier that has added the most capacity to these trades, up 54% from a year ago and adding almost 490 000 TEU.

About half of this capacity has been deployed on MSC’s standalone services, while the rest has been deployed on 2M services.

This has allowed 2M to grow its share of capacity between Asia to Europe, rising to 33%, while also increasing the share of non-alliance capacity, rising to from 5% last February to 11%.

The EU commission has approved CMA CGM’s USD 5.2 billion takeover of Bolloré Logistics.

This adds to CMA CGM’s existing portfolio which already includes CEVA, acquired back in 2019.

With this latest acquisition CMA estimates it will become the world’s fifth largest global logistics company.

Both CMA CGM and Maersk have spent a lot of time and money on widening their footprint on the global logistics scene in hope of stabilizing revenue away from the volatile ocean freight market.

However, there are big differences in how the two companies have gone about this.

CMA CGM has kept CEVA as a subsidiary, maintaining its brand, which Bolloré will likely now join.

In contrast, the many specialized and regional freight forwarders Maersk has acquired have been brought in-house under its integrator model.

This has led to tensions with traditional freight forwarders who see Maersk as a competitor, whereas by splitting its departments, CMA CGM may avoid this negative perception.

OCEAN OBSERVATION

Retailer expands ocean business

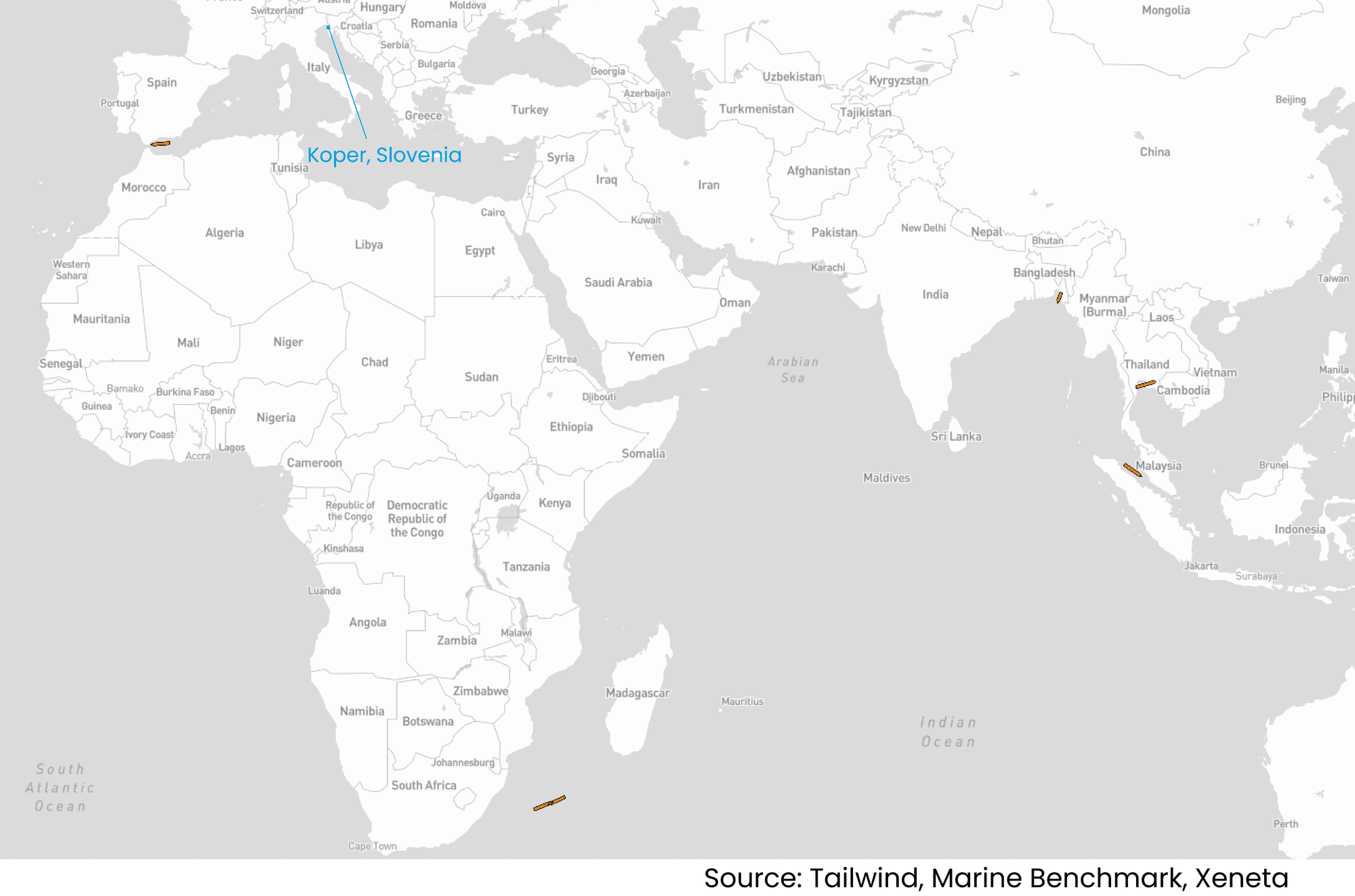

A much smaller ocean carrier, Lidl’s Tailwind, which was set up in April 2022 when the German retailer was struggling to get space on traditional carriers’ ships, has announced it will expand into hinterland logistics.

Though Tailwind Intermodal will operate with a very narrow geographical scope, focusing on goods coming in through the Slovenian port Koper, this further step into the logistics game is in contrast to other retailers who chartered ships at the peak of the pandemic, but have since left the market.

The graphic identifies vessels currently owned by Tailwind.

The question of when a crisis is over is becoming increasingly relevant as container shipping has once again proved its adaptability in the face of the escalation of conflict in the Red Sea.

With the spot market softening, some shippers are now looking to renegotiate rates signed even just a few weeks ago, with others pushing hard for the phasing out of crisis-related surcharges.

This is the case even as most carriers are still avoiding the Red Sea, with only CMA CGM saying it will return to the region.

The attacks on ships by Houthi Rebels have continued, targeting other ship types that have continued to transit the Red Sea, as well as hitting the MSC Sky II on 4 March.

This container ship was not sailing through the Bab al-Mandab Strait, but was hit south of Yemen as it sailed from Singapore to Djibouti.

Away from container shipping, a missile strike on a Greek-owned but Barbados flagged bulk ship has reportedly resulted in the death of three seafarers.

These are the first deaths caused by the Houthi’s attacks on commercial ships.

Hard negotiations for new contracts

Despite continued attacks in the Red Sea the market is clearly softening, which presents a dilemma to the many shippers entering their tender season.

Carriers at TPM, which took place in California this week, will be keen to point towards increases in the spot market since December, which, even with the market softening since early February, are considerable.

Then there is also the rise in the Global XSI® in February, which measures all valid long term contracts in the market.

Shippers on the other hand will be focusing on falling spot rates and overcapacity in the market – which will only grow as more new ships hit the water this year.

OCEAN OUTLOOK

How to navigate these waters will depend on each shipper’s individual profile and needs, but all should consider the risks of signing a 12 month contract now.

Barring another Black Swan event, the market will continue to fall, which shippers will lose out on if they lock in long-term rates for the next 12 months.

Looking instead at shorter contract lengths, choosing index linked rates or perhaps delaying new negotiations may prove a better solution.

A poll during a recent Xeneta customer webinar showed a 10 percentage point drop in shippers negotiating contracts for one year, and a 10 percentage point increase in those negotiation for three to six months.

Xeneta is the leading ocean and air freight rate benchmarking, market analytics platform and ocean container rate index, Xeneta Shipping Index (XSI®).

Xeneta’s powerful reporting and analytics platform and data density provide liner-shipping stakeholders the insights they need to understand current and historical market behavior – reporting live on market average and low/high movements for both short and long-term contracts.

Xeneta’s data is comprised of over +400 million contracted container rates and covers over 160,000 global trade routes. Xeneta is a privately held company with headquarters in Oslo, Norway and regional offices in New York and Hamburg. To learn more, please visit www.xeneta.com

NOTE: The XSI® public indices reports are based on long-term contracts only.

© 2024 Xeneta AS

Quarterly Market Average, 40' Container

Monthly Market Average, 40' Container

Quarterly Market Average, 40' Reefer HC