Market News By Xeneta

February 26, 2024

Market News by Xeneta Feb 26, 2024

Visit Xeneta Customer Portal

(IQ Hub) For

Exclusive Market Content

OCEAN RECAP

Carriers appear to be losing the battle to keep rates elevated out of the Far East.

They have been unable to implement more GRIs on the major trades since the round on 1 February – and even then they were unsuccessful in raising rates between the Far East and Europe.

With Lunar New Year behind us and, dare we say it, carriers and shippers settling into a new normal with diversions in the Red Sea, spot rates are now softening.

For example, between the Far East and the Mediterranean, the trade on which ocean freight shipping costs increased the most during the Red Sea crisis, rates are now down by 10.7% from their peak in mid-January

Spot rates from the Far East to the US have followed the developments on trades into Europe, but with a 15 day lag.

Despite rates starting to soften on European trades, carriers still attempted to push through another round of GRIs in mid-February which proved unsuccessful.

For example, spot rates from the Far East into both US coast are down from the Red Sea crisis peak in early February.

Market average rates do not always translate into the average revenue a carrier makes per box.

This is an important distinction in the current climate because the market mid low and low rates, which are typically occupied by high volume shippers, have increased.

For example, the market low on spot rates from the Far East to North Europe is up by 150% compared to three months ago at USD 2 450 per FEU. This is almost USD 1 000 higher than the market average on this trade at the start of December 2023.

While it is therefore true that carriers are seeing the average spot rates soften, their revenues could be insulated through the large volume shippers paying more overall.

There is more reason for carriers to find some solace because, even though rates are softening, they remain more than double (and on some trades triple) what they were three months ago.

2024 was also supposed to be the year of continued overcapacity and financial woe for carriers who had already posted big drops in revenue and profits in Q4 2023. Against that background, carriers will grab hold of any opportunities that come their way.

Better news for shippers can be found on the long term market.

Though many shippers are seeing new surcharges being applied to their previously agreed rates, the market average has not seen anywhere near the same increase as on the spot market.

OCEAN OBSERVATION

Now past the pre-Lunar New Year rush in demand, carriers are adapting to the longer transit times caused by Suez Canal diversions around the Cape of Good Hope and looking to fill the holes in their schedule caused by ships heavily delayed returning to the Far East.

Carriers are achieving this by increasing sailing speeds and omitting certain port calls to limit delays.

In some cases port calls in Northern Asia have been removed, meaning shippers in those regions are having to use feeder services to get their containers to a port at which the main trade is still calling.

In other cases, carriers are omitting direct port calls in the Mediterranean, unloading containers in Tangier or at more northern ports and then transshipping them into the Mediterranean and onwards to their intended destination.

Overcapacity, which many believed would be the financial albatross around carriers’ necks during 2024, has actually helped them deal with the impact of the Red Sea diversions.

There have been 57 new ships delivered into the container fleet so far this year, totalling 396 000 TEU.

17 of these ships have a capacity over 13 000 TEU, and 11 of which have been deployed straight onto Far East to Europe or US East Coast trades.

Some carriers and alliances have benefitted more than others.

MSC has added six of these 13 000+ TEU ships with its alliance partner Maersk receiving another two.

One of these two ships – the Ane Maersk – is notable for being the first large container methanol-capable ship to be delivered (though a steady supply of methanol has yet to be secured for its operations).

In contrast, THE OCEAN Alliance has only seen the addition of one of these new ultra large container ships delivered to its current members, namely Hapag-Lloyd.

After trending upwards through the second half of 2023, the idle fleet has also dropped, falling to 0.7% on 12 February according to Alphaliner.

Carriers have turned to the charter market to secure these extra ships, which in turn has caused charter rates to rise.

The question now facing carriers is how long to charter these ships for, balancing the need to agree terms with the ship owner in a market of low supply against paying too much or committing for too long a period.

OCEAN OUTLOOK

Unlike during Covid-19 when disruption was caused by increasing demand for ocean freight, the Red Sea diversions is an issue of available capacity.

Although there has not been an impact on the number of containers being moved, they are now being transported over longer distances.

However, the container shipping fleet is more than capable of meeting this additional need, leaving very different market dynamics than those in 2021/2022.

Since the start of 2022 the container shipping fleet has grown by 13.6% (2024 YTD), whereas container volumes in 2023 were 3.8% lower than in 2021. An imbalance that will widen this year, as Xeneta expects the fleet to grow by around 6.5%, compared to demand growth in the region of 2.5%.

Barring further black swan events, this means spot rates are likely to keep falling from their current levels, though a return to Q4 2023 rates still seems some way off.

Perhaps more importantly for stakeholders heading to TPM 2024 at the start of March is the market moving on from widespread uncertainty caused by the sudden escalation in the Red Sea conflict, which saw shippers paying whatever rate necessary to secure space on board.

If the market is now seeing carriers unable to push through GRIs and heading into negotiations with US shippers with overcapacity on their minds, it could be an interesting couple of months.

Xeneta's iXRT report provides our customers with valuable ocean and air freight insight - and it's getting even better in 2024.

Future editions of the iXRT will be dedicated to either ocean or air on an alternating basis, rather than the current combined report. That means we can bring you even greater levels of insight on the markets that matter most. The new iXRT reports will be published approximately every two weeks.

This means the first dedicated iXRT Ocean report will be published on 7 February, with the first dedicated Air iXRT report following on 21 February.

AIR RECAP

Any suggestion of a post-Christmas drop in e-commerce traffic was countered by shippers’ concerns over hostilities in the Red Sea and Lunar New Year as global air cargo volumes increased by 10% year-on-year in January.

While this increase may have come as a surprise to some, with plenty of air cargo capacity in the market during this traditionally quieter time of year, these fuller cargo holds have not yet translated into higher rates.

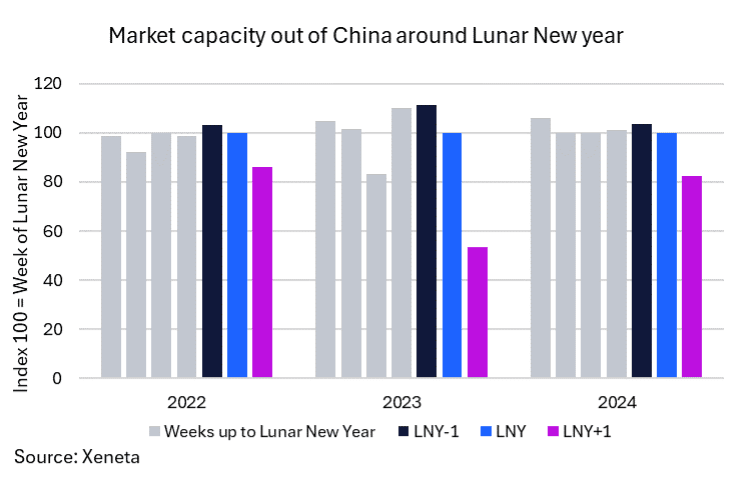

Looking a little closer at capacity, Lunar New Year fell later this year than in both 2023 and 2022 and with the Red Sea crisis there has been a bigger focus on air freight.

But, if we look at capacity out of China to the rest of the world in the weeks leading up to Lunar New Year and the week after, there are some noticeable differences.

This year, the week following Lunar New Year (LNY+1) is down 20.3% from the week prior to Lunar New Year (LNY-1).

Last year the change between LNY-1 and LNY+1 was much higher at -52%.

However, if we look back to 2022, we see the change between LNY-1 and LNY-2 was -16.4%, which suggests 2024 is not so much of an outlier as would first appear.

Globally, general air cargo spot rates in February remained flat compared to January at an average USD 2.24 per kg, while the dynamic load factor increased by 4% points to 61%.

Overall, the year-on-year growth of global air cargo market supply has slowed down in January and February to date due to the restoration of capacity during 2023.

Compared to the previous year, February’s global average spot rate continued to show a double-digit year-over-year decline of -14%.

Data for the full month of February will be available next week and it will be intriguing to see what impact there has been on spot rates – this will be covered in the next Xeneta iXRT report.

We saw a relatively strong January from a volume perspective, but the market fundamentals have not changed.

This is not a case of consumers buying more, it is partly linked to Red Sea disruption as well as the Lunar New Year and some indicators that the general cargo market is busier than expected.

AIR OBSERVATION

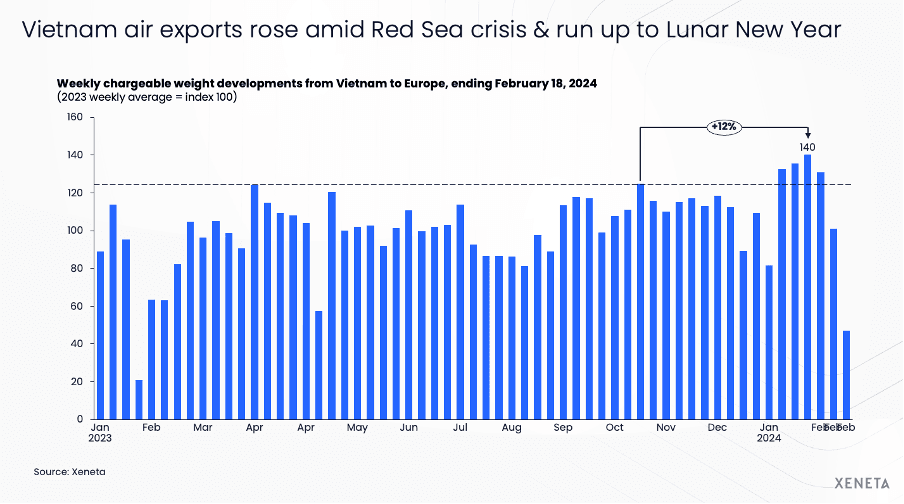

In the third week of January we reported on the surge of volumes from Vietnam to Europe as a result of the Red Sea Situation and the run up to the Lunar New Year.

This trend continued until the first week of February, after which the volumes declined as factories started to wind down for the upcoming holiday season.

Similar to what we have seen at the Global level, this increase in volumes did not result in an increase in rates. Spot rates have been hovering around the USD 3.30 / kg since the turn of the year.

The flights connecting the Vietnam production facilities and European consumers have been full (from a cargo perspective) since the start of the year, with an average load factor value of 92%. Only in the second week of February did it drop to 85%, reflecting slowed demand.

AIR OUTLOOK

Although it might not feel that way to people living in the Northern Hemisphere, spring is just a few weeks away.

Next to the increasing temperatures, this will also result in a rise in belly capacity across the Atlantic as airlines start introducing summer schedules for passenger flights in the last week of March.

We would expect to see a capacity increase of 20-30% on this trade lane relative to the current winter schedule.

As demand can seldom keep up with such an increase in supply, a drop in overall load factors of 10-15% will be the likely result.

It remains to be seen what the overall impact on rates will be - not so much on the downwards direction, but more the order of magnitude.

The jet fuel spot price in US Gulf has been trending upwards all year hitting USD 2.86 per gallon in mid February.

The average in February is just 2.1% lower than the corresponding month last year, though still below the peak in prices in Q3 2023.

Xeneta is the leading ocean and air freight rate benchmarking, market analytics platform and ocean container rate index, Xeneta Shipping Index (XSI®).

Xeneta’s powerful reporting and analytics platform and data density provide liner-shipping stakeholders the insights they need to understand current and historical market behavior – reporting live on market average and low/high movements for both short and long-term contracts.

Xeneta’s data is comprised of over +400 million contracted container rates and covers over 160,000 global trade routes. Xeneta is a privately held company with headquarters in Oslo, Norway and regional offices in New York and Hamburg. To learn more, please visit www.xeneta.com

NOTE: The XSI® public indices reports are based on long-term contracts only.

© 2024 Xeneta AS

Quarterly Market Average, 40' Reefer HC

Monthly Market Average, 40' Container

Quarterly Market Average, 40' Container

500kg - Long Term Rates