Air Market News By Xeneta

May 27, 2024

Market News by Xeneta May 27, 2024

Visit Xeneta Customer Portal

(IQ Hub) For

Exclusive Market Content

The Xeneta Air iXRT provides an overview of market movements, the key risks and issues to be aware of and insight on how these may develop in the coming weeks and months.

Topics covered in this edition of the iXRT Air include:

Global air cargo spot rates start to show signs of decline.

Flattening air cargo demand on the Transpacific market.

Increase in newly contracted long-term rates for the top three global air cargo corridors.

Fuel surcharges fall by around 20% in May compared to 2023

E-commerce demand from China means busy air cargo peak season.

Strong exports observed from India and mainland China.

AIR RECAP

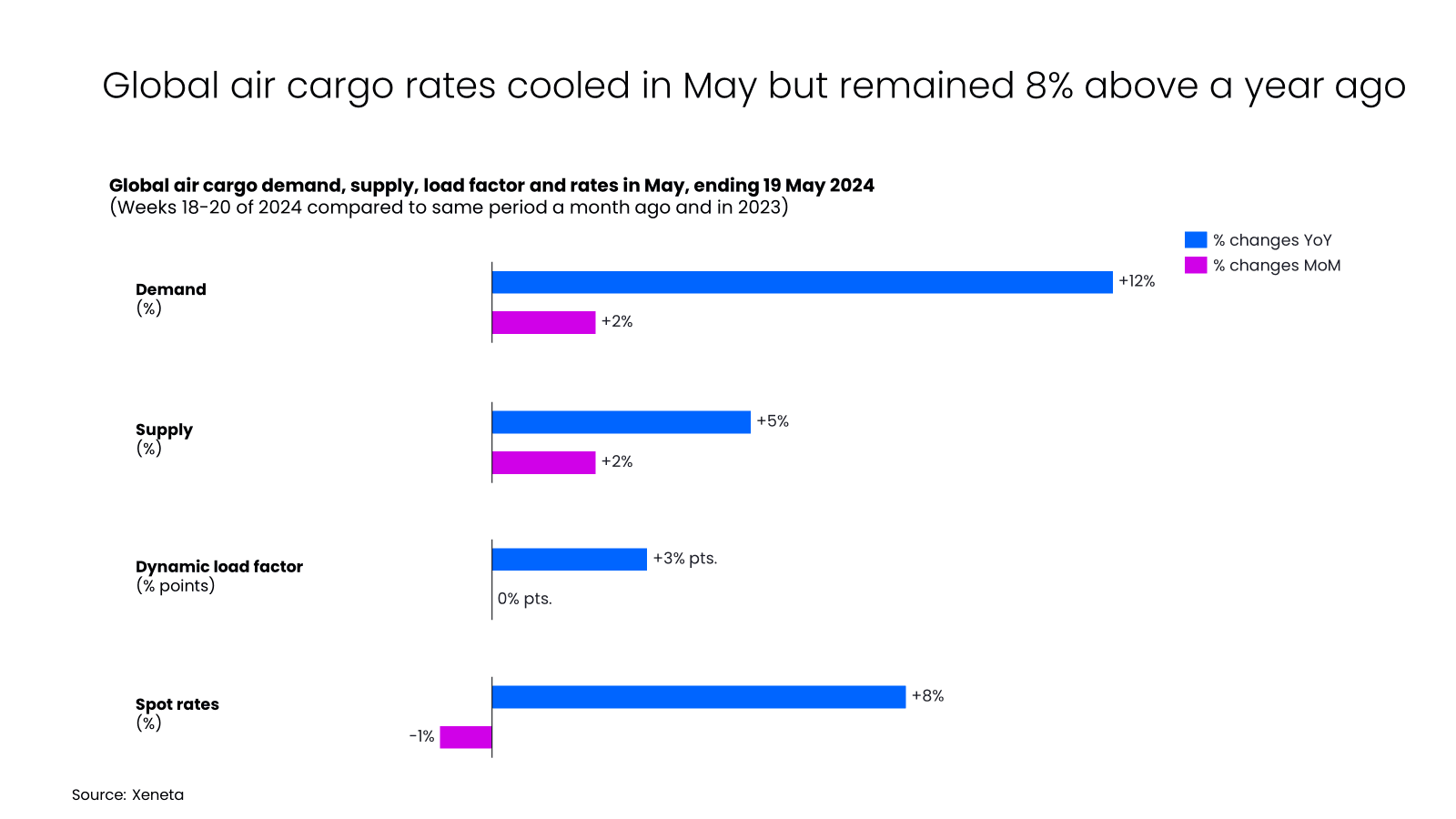

Following two consecutive months of high-single-digit growth, the global air cargo spot rates have started to show signs of decline, edging down 1% month-on-month so far in May.

Additional capacity from airline summer schedules on the Transatlantic market has contributed to this freight rate decline.

Coupled with a low-single-digit decline in demand, the air cargo spot rate from Europe to North America May-to-date is down 8% compared to a month ago.

In addition to the increased capacity due to summer schedules, the freight rate decline is also attributed to the reduced pressure from the Red Sea disruptions.

As shippers have been adjusting their supply chain to cope with longer voyages and additional sailing time in ocean freight services, the need for air freight has become less.

The Red Sea disruptions saw air cargo volumes from the Middle East and Central Asia to Europe increase by nearly 70% year-on-year at its peak at the end of February. However, by mid-May the cargo spot rate was down 1% month-on-month.

On the Asia Pacific to Europe and Middle East Market, geopolitical tensions continue to exert upward pressure on air cargo rates. This has seen a low-digit uptick in spot rates May-to-date due to a small increase in demand growth while supply remained steady.

Another factor contributing to the global freight rate decline is flattening air cargo demand on the Transpacific market in May.

The ongoing surge in e-commerce demand on this trade managed to counterbalance volume declines in other sectors, leading to the cargo spot rate flattening out.

Hong Kong to North America is the only major Transpacific route to experience an increase (+4%) in cargo spot rates May-to-date.

The Latin America to North America market is perhaps the only major corridor to see significant air cargo spot rate growth. Driven by Mother's Day floral demand, the average air cargo spot rate increased by 11% May-to-date, compared to a month ago.

Although the global air cargo spot rate ticked down month-on-month, the average spot rate May-to-date is up 8% compared to the same period a year ago.

This is because the global air cargo market has seen demand growth (+12% year-on-year) outpace supply growth (+5% year-over-year).

Factors such as increased e-commerce and floral volumes, as well as ongoing disruptions in the Red Sea fueled this growth in air cargo demand.

Furthermore, the jet fuel cost – one of the largest cost components for airlines – could also contribute to this rate increase.

The airline fuel model often reflects the fuel movement in the previous period. For example, a 10% year-on-year increase in the April US Gulf Coast kerosene-type spot rate may result in higher fuel surcharges for May if airlines cannot absorb them.

This could further accelerate the year-on-year growth in airline spot rates.

AIR OBSERVATION

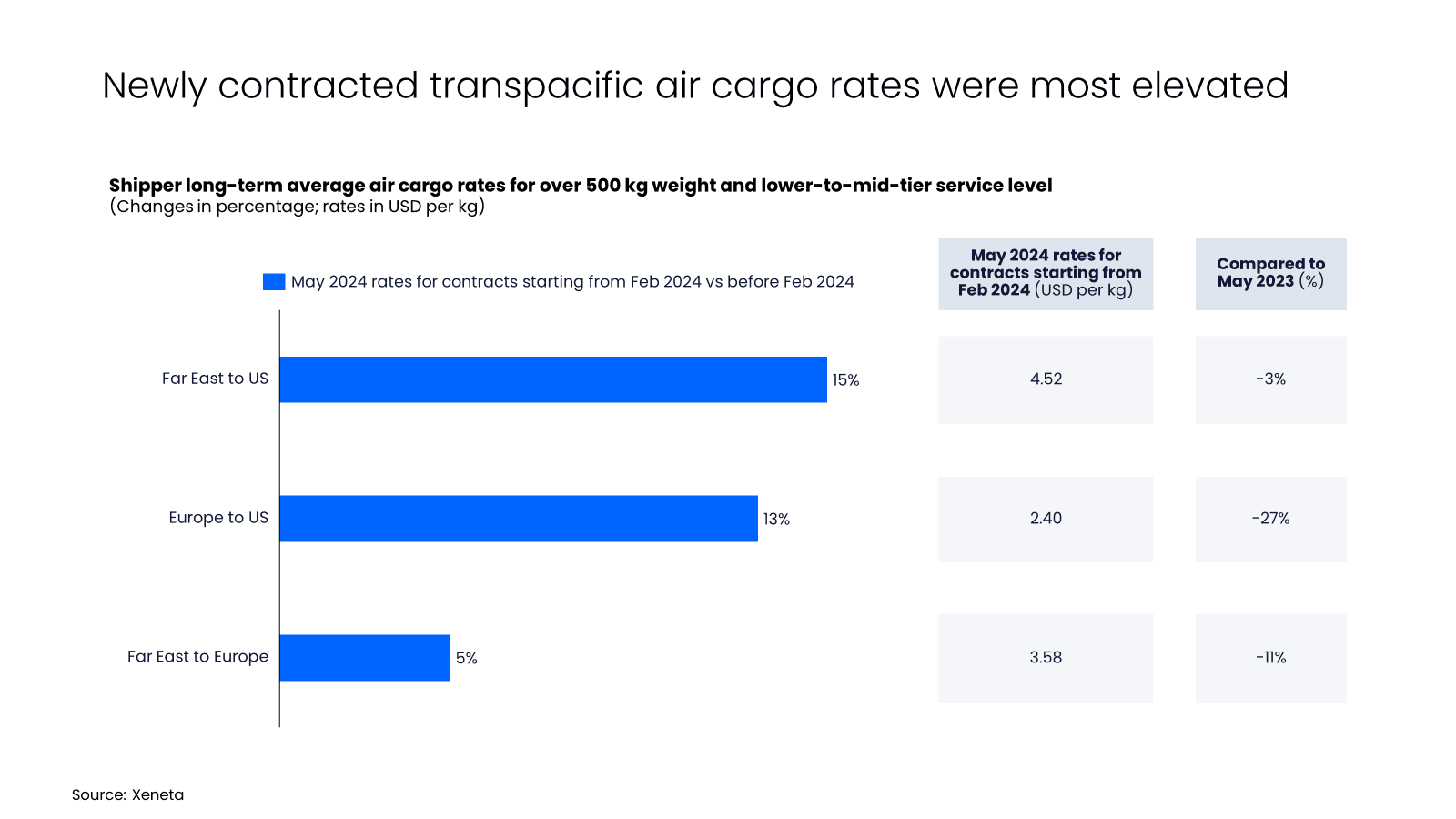

The impact of freight rate increases at the beginning of the year has also been felt by shippers.

In May, shippers’ newly contracted long-term rates (with contracts starting from February) for the top three global air cargo corridors – Far East to the US, Far East to Europe, and Europe to the US – were higher when compared to those contracted before February.

The Red Sea disruptions and surging e-commerce demand fueled these increases, with the new long-term rates up by 5-15% compared to the ones contracted before February.

The modest 5% increase in long-term rates from the Far East to Europe since February can be attributed to the growth occurring from an already high base.

As of May, these rates were over 40% above their pre-pandemic levels.

This contrasts with the markets from Europe to the US and from the Far East to the US, where May long-term rates were only about 20% higher than pre-pandemic levels.

The largest increase in newly signed long-term rates is found on the Far East to US market, up by 15%, and is likely driven by a positive outlook for the e-commerce section and a resilient US economy.

However, the aforementioned annual growth in airline spot rates has not yet been fully reflected in the long-term rates paid by shippers.

In May, the newly contracted shipper long-term rates (contracts starting from February) on the top three corridors continued to decline, down by between 3% and 27% compared to the levels during the same period in 2023.

The year-on-year decline in shipper long-term rates reflects the continued normalization of the market, with the expectation that the summer cargo capacity growth surpasses demand growth.

The other contributing factor to the decline in shippers’ long-term rates is the decrease in fuel surcharges, which fell by around 20% in May compared to the same period in 2023. This is in contrast to the 10% spike in jet fuel costs in April, hinting that the fuel costs were not fully transferred to the shippers.

AIR OUTLOOK

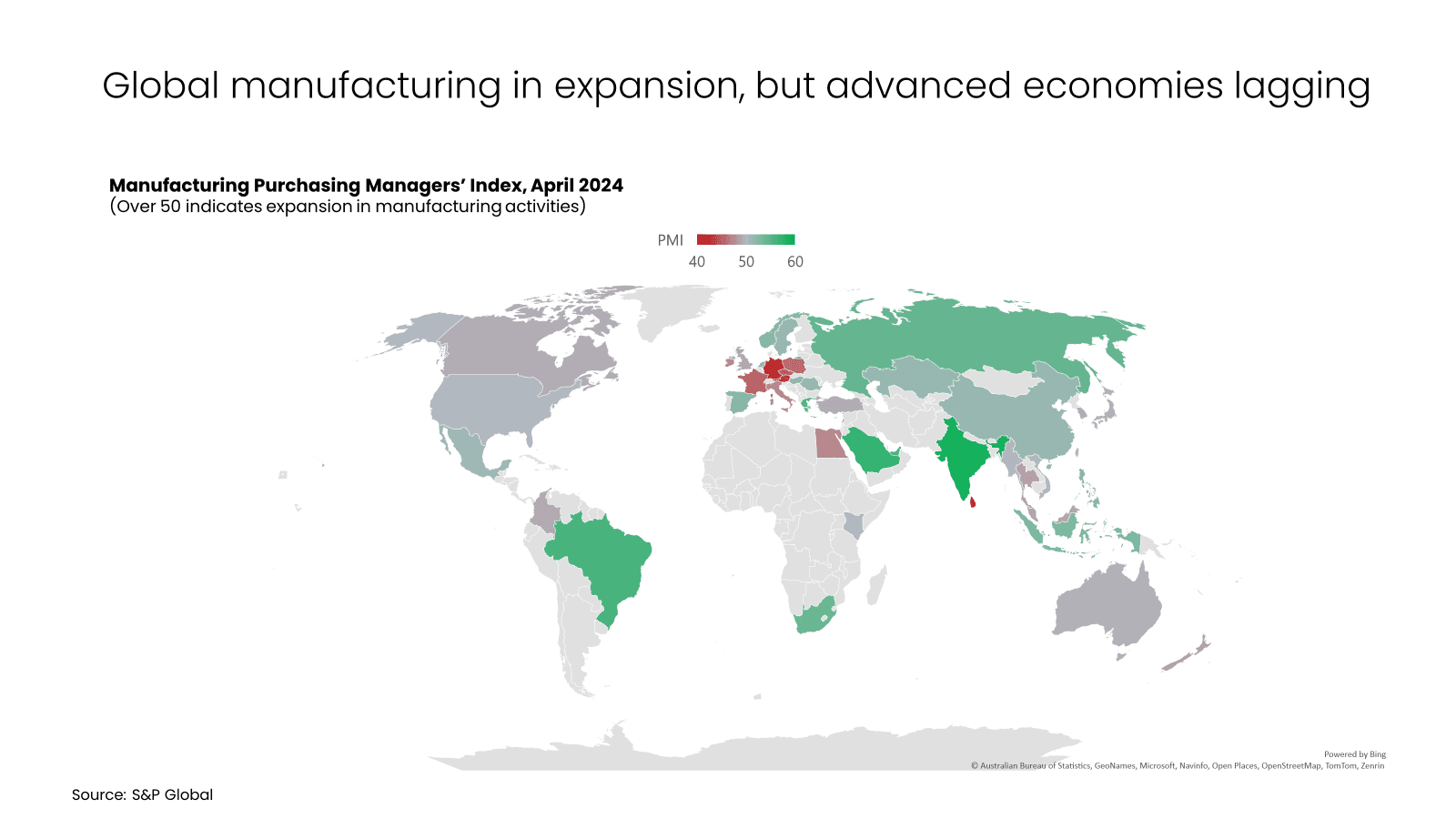

Signals from across the global economic landscape along with the surge in e-commerce demand from China means 2024 is likely to end with another busy air cargo peak season.

For instance, the global manufacturing purchasing managers’ index – a bellwether for global trade and air cargo demand – remained in expansion mode in April (source: S&P Global).

China, a global manufacturing powerhouse, continued to expand its manufacturing activities, with similar trends observed in other major regional economies, such as India, Saudi Arabia and Brazil.

The sub-index for new export orders returned to growth after more than two years of decline. The strongest exports were observed from India and mainland China, while the declines were mainly seen in Europe.

One concern, however, is the escalation of input costs, primarily due to rising labor costs. This increase could elevate selling prices in the months ahead and potentially dampen demand.

Additionally, US President Biden’s recent announcement of new tariffs on Chinese imports will renew concerns over the potential for an escalation in the trade war between the two nations. The new tariffs will apply to USD 18 billion of Chinese goods including electric vehicles, semi-conductors and solar cells.

This may not cause significant disruption in the immediate future compared to the tariffs imposed by the Trump administration in 2018-2019. The USD 18 billion worth of goods accounts for only a fraction of the nearly half a trillion dollars of goods imported into the US from China in 2023.

Additionally, not all tariffs will come into effect in 2024, with some only becoming effective in 2025 and 2026.

Xeneta is the leading ocean and air freight rate benchmarking, market analytics platform and ocean container rate index, Xeneta Shipping Index (XSI®).

Xeneta’s powerful reporting and analytics platform and data density provide liner-shipping stakeholders the insights they need to understand current and historical market behavior – reporting live on market average and low/high movements for both short and long-term contracts.

Xeneta’s data is comprised of over +450 million contracted container rates and covers over 160,000 global trade routes. Xeneta is a privately held company with headquarters in Oslo, Norway and regional offices in New York and Hamburg. To learn more, please visit www.xeneta.com

NOTE: The XSI® public indices reports are based on long-term contracts only.

© 2024 Xeneta AS

Long term rates contracted within the last 3 months