Air Market News By Xeneta

June 24, 2024

Market News by Xeneta Jun 24, 2024

Visit Xeneta Customer Portal

(IQ Hub) For

Exclusive Market Content

The Xeneta Air iXRT provides an overview of market movements, the key risks and issues to be aware of and insight on how these may develop in the coming weeks and months.

Topics covered in this edition of the iXRT Air include:

Upward pressure on rates during summer

Increased scrutiny on e-commerce

Contracts more than six prove most popular

Impact of turmoil in ocean container shipping

Further decline in US retail sales

Risk with potential labor strikes at US East Coast ports

AIR RECAP

The summer season in the northern hemisphere has traditionally been the time when the air cargo market cools down, whereas, somewhat paradoxically, it is during the winter when freight rates start to heat up.

This year, things are a little different with the global air cargo market seemingly on course to avoid a cooler summer.

In fact, the global average air cargo spot rate held steady in the first half of June, up 1% compared to a month earlier.

AIR OBSERVATION

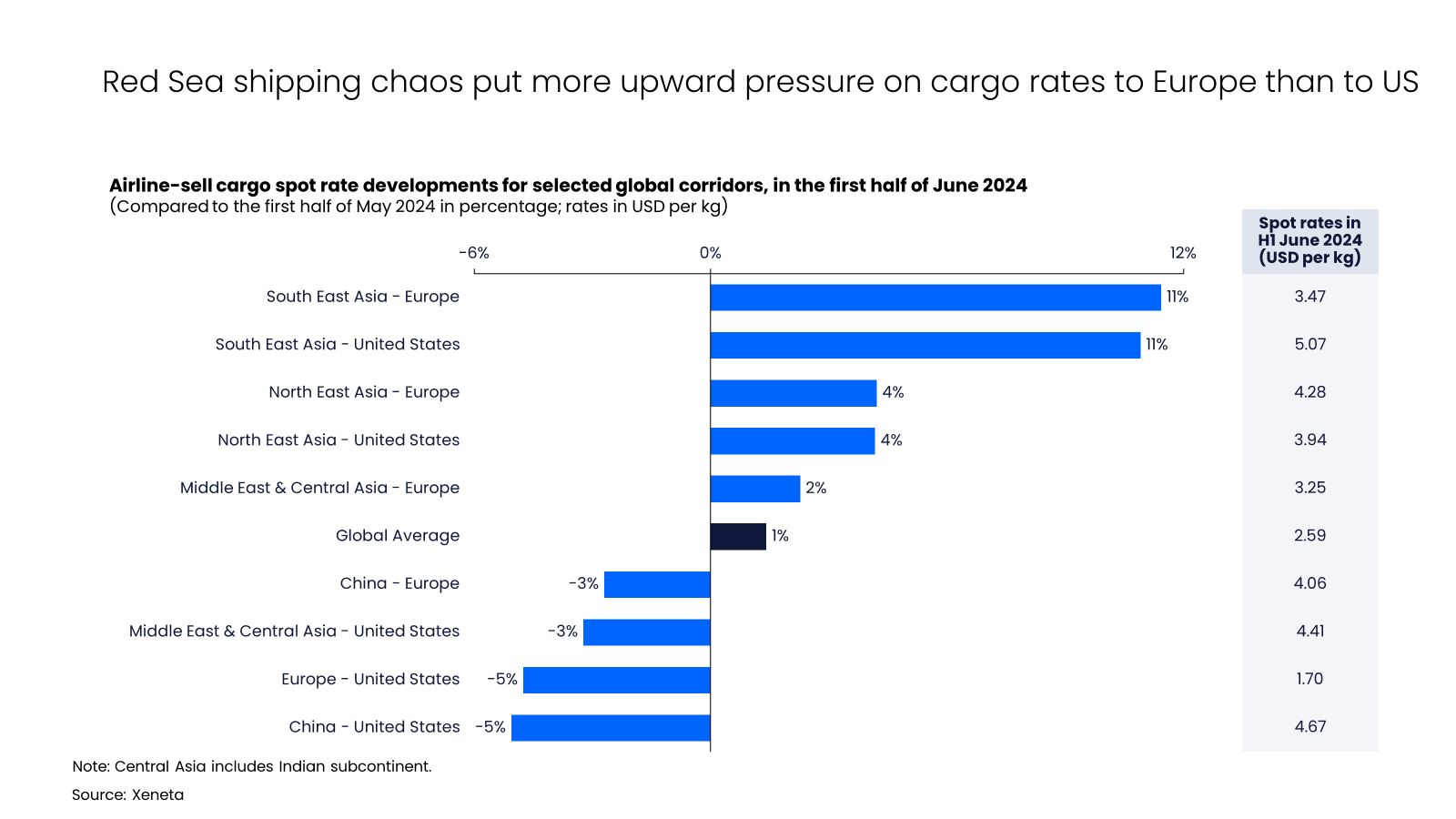

Ongoing disruption to ocean freight container shipping due to the conflict in the Red Sea region has continued to put upward pressure on air cargo rates from Asia to Europe.

In the first half of June, the Southeast Asia to Europe market led the spot rate growth, up 11% compared to a month earlier.

This was followed by the ex-Northeast Asia market (excl. China) and Middle East & Central Asia, which showed 4% and 2% growth respectively.

During the same timeframe, outbound China was the only major market to see a slight spot rate decline of 3%.

On the other hand, air cargo markets not directly impacted by the Red Sea region demonstrated some traits of classic summer seasonality.

Thanks to an influx of belly capacity, air cargo spot rates from Europe to the US in the first half of June dropped 5% from a month earlier.

Meanwhile, the spot rates from China and Middle East & Central Asia to the US cooled off, down 5% and 3% respectively.

But the Northeast Asia (excl. China) and Southeast Asia to the US markets remained buoyant.

Air cargo spot rates originating from Northeast Asia and Southeast Asia to the US grew at a similar pace to the inbound Europe rates, up 4% and 11% respectively compared to a month earlier.

Whatever one's thoughts are on the booming e-commerce trade out of China, it is now receiving more attention from the US and EU authorities.

In late May the US Customs and Border Protection announced it is stepping up its enforcement to ensure compliance and minimize exploitation, such as counterfeits and undervaluation, in small parcels.

Several customs brokers have been suspended from participating in the Entry Type 86 Test — an electronic entry type to import small shipments without paying duties and taxes under de minimis environment — after posing a non-compliance risk.

On the other side of the Atlantic Ocean, Temu is also facing stricter compliance rules after the EU designated it as a Very Large Online Platform under its Digital Services Act in late May.

This decision follows a recent analysis from the European Commission that nearly 65% of parcels entering the EU are undervalued.

So far, the impact of increased e-commerce scrutiny seems limited, with outbound Hong Kong and Southeast China cargo rates holding steady in the first half of June.

Despite rumors of paused outbound China charters and congestion at major air freight hub LAX, the increased checks on US imports have yet to disrupt freighter activities.

What if the US starts to lower its de-minimize threshold? Such attempts are unlikely to dull consumer appetite for cheap goods.

The EU, for instance, has a much lower de minimize threshold of EUR 150 (roughly USD 160) compared to the US threshold of USD 800, but still continues to grapple with rising e-commerce demand.

While protectionist measures like import tariffs on Chinese goods might temporarily curb demand, they may also simply prompt a shift in production to other countries and imports will continue unabated.

A complete removal of the de minimize threshold could eventually be introduced.

In 2023, the EU proposed a customs reform which includes the abolishment of its current de minimize threshold.

However, the timeline of 2028 for e-commerce companies and 2038 for all other businesses still feels a long way off.

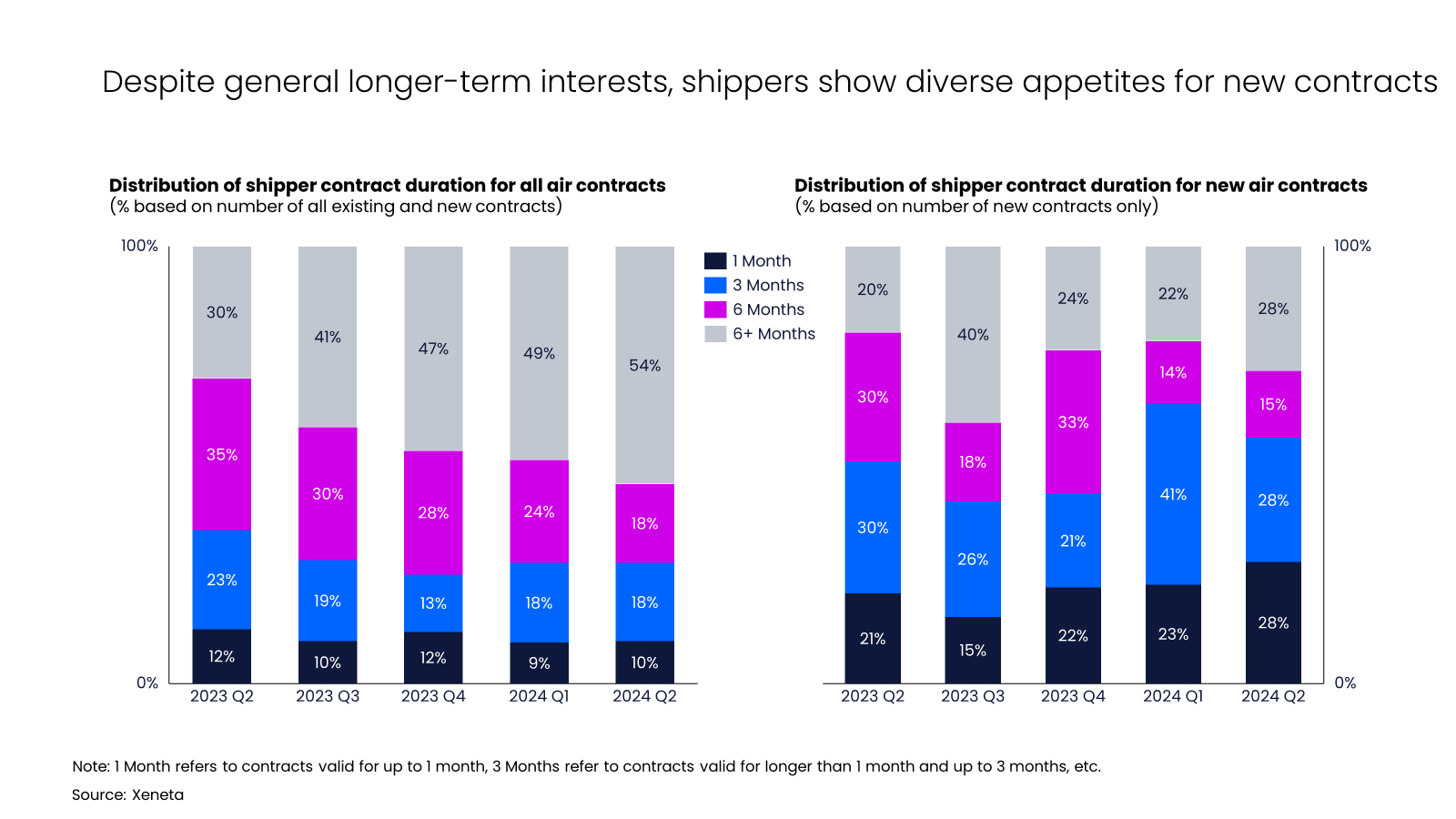

It’s time for Xeneta’s quarterly review of shippers’ appetites regarding air cargo contract lengths. In the second quarter of 2024, contracts lasting more than six months continued to top the list, now accounting for 54% of the total market.

This is at the expense of appetite for half-year contracts, which fell 6 percentage points to 18% of the total market.

The increased interest in contracts lasting more than six months compared to half-year contracts suggests shippers are eager to lock their cargo rates for the upcoming year-end peak season.

The same appetite is reflected in newly signed contracts valid from Q2. Contracts lasting more than six months again top the list, with an increasing market share of 28%.

However, the top spot is shared with three-month and one-month contracts which also hold 28% of the market share.

The growing proportion of one-month contracts suggests increased pressure in maintaining longer-term contracts during periods when freight forwarding procuring rates are rising.

Meanwhile, the shrinking three-month contracts point to anxiety over renegotiating contracts just before the year-end peak season.

This is a clear demonstration of shippers adopting diverse strategies in order to navigate the diverse current market.

The same appetite is reflected in newly signed contracts valid from Q2. Contracts lasting more than six months again top the list, with an increasing market share of 28%. However, the top spot is shared with three-month and one-month contracts which also hold 28% of the market share.

Is a fresh air cargo boom under way? The air freight surges around the Red Sea region, as discussed in the Recap section, are more a reflection of the way the market responds to supply chain stress in ocean container shipping, rather than real underlying growth in consumer demand.

In response to enduring low shipping schedule reliability, port congestion and container shortages, shippers are frontloading imports to build up inventories ahead of the ocean peak season in Q3. Any easing in this approach could have an impact on air freight.

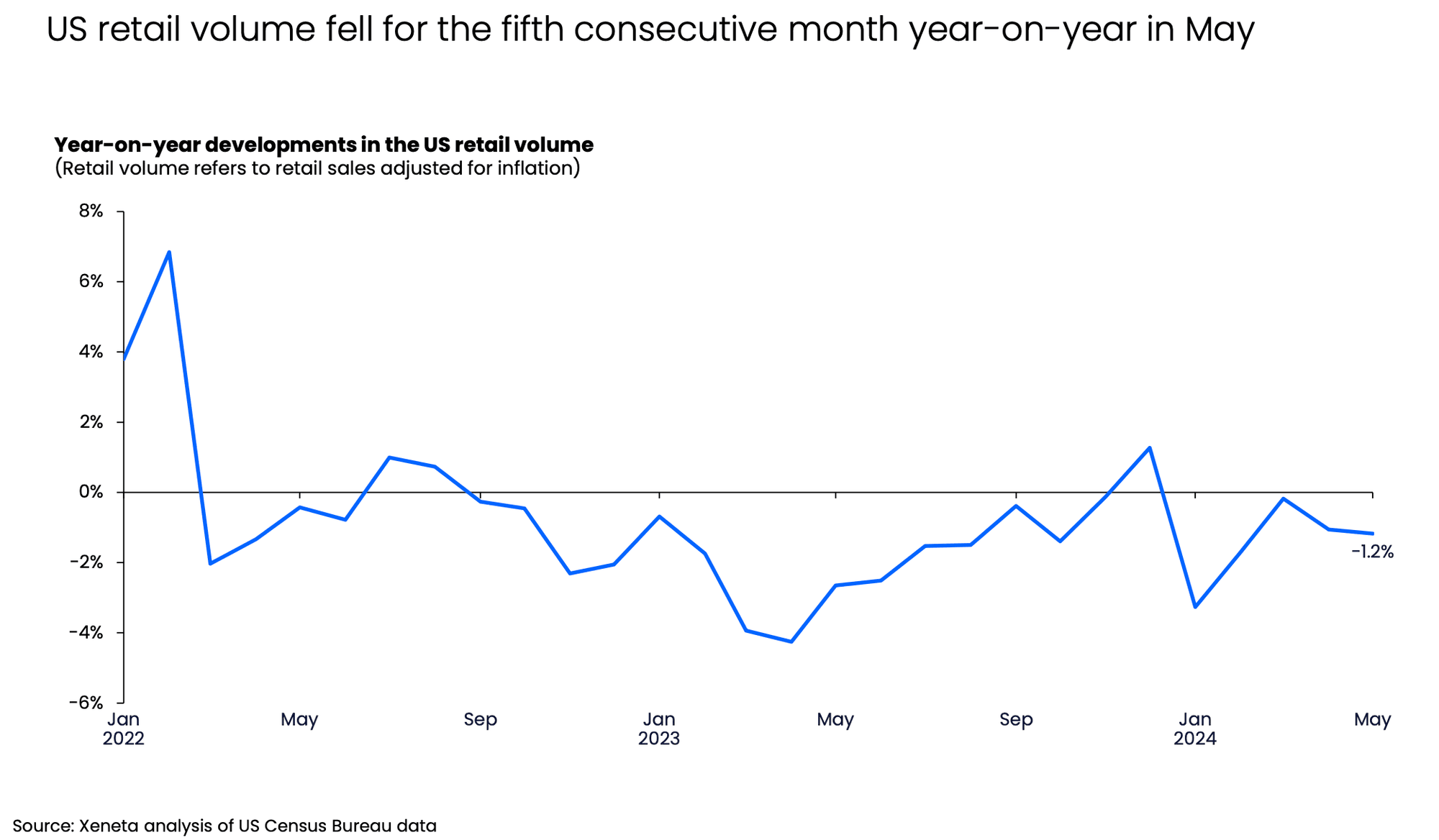

In addition, US retail sales in May showed a fifth consecutive month of year-on-year decline (-1.2%) after adjusting for inflation (source: US Census Bureau). This points to a weak consumer demand, which is unlikely to support continued growth in general freight demand.

A further complication may arrive in the form of potential labor strikes at US East Coast and Gulf Coast ports.

This disruption could trigger a shift from ocean to air freight services and put upward pressure on air cargo rates.

However, its impact is likely to be less severe than the 2014-15 US West Coast strike because this time, shippers can import into the US West Coast and use intermodal transport services to get their goods to the Eastern US.

E-commerce out of Asia remains an important driver for air cargo demand.

However, increasing scrutiny on this business model does raise question marks in the longer term if it disrupts cargo flow or dampens demand.

Will there be an air cargo boom? The answer may well lie in the evolving picture in ocean freight shipping in the coming months.

AIR OUTLOOK

Xeneta is the leading ocean and air freight rate benchmarking, market analytics platform and ocean container rate index, Xeneta Shipping Index (XSI®).

Xeneta’s powerful reporting and analytics platform and data density provide liner-shipping stakeholders the insights they need to understand current and historical market behavior – reporting live on market average and low/high movements for both short and long-term contracts.

Xeneta’s data is comprised of over +450 million contracted container rates and covers over 160,000 global trade routes. Xeneta is a privately held company with headquarters in Oslo, Norway and regional offices in New York and Hamburg. To learn more, please visit www.xeneta.com

NOTE: The XSI® public indices reports are based on long-term contracts only.

© 2024 Xeneta AS

Long term rates contracted within the last 3 months