Air Market News By Xeneta

Apr 23, 2024

Market News by Xeneta April 23, 2024

Visit Xeneta Customer Portal

(IQ Hub) For

Exclusive Market Content

The Xeneta Air iXRT provides an overview of market movements, the key risks and issues to be aware of and insight on how these may develop in the coming weeks and months.

Topics covered in this edition of the iXRT Air include:

Global air cargo spot rates begin to ease

Global demand drops in first two weeks of April

World's top 10 busiest cargo airports revealed

Conflict and floods in the Middle East

Uncertainty impacts freight forwarder strategy

Spot share declines on major trades

AIR RECAP

Growth in the global air cargo spot rate has finally started to ease after flattening at USD 2.61 per kg in the weeks ending 7 April and 14 April.

These two consecutive weeks of flattening rates follow the market reaching a low of USD 2.25 per kg in the last week of February.

There is also evidence the general air cargo market may be entering a quieter summer period after global demand in the first two weeks of April fell 7% compared to the same period one month ago. It is likely rates will react and come down soon.

Increased belly capacity due to airlines’ summer schedules is also relieving the upward pressure on freight rates.

The Europe to US corridor led the decline in the global air cargo spot rate, with a week-on-week drop of 6% in the week ending 14 April, accelerating from a 5% decline the previous week.

The spot rate from China to Europe remained unchanged in the week ending 14 April at USD 3.91 per kg, while the rate from China to US dipped slightly to USD 4.44 per kg, down from USD 4.47 per kg a week earlier.

However, the spot rates into Europe and North America from Southeast Asia, the Middle East and Central Asia continued to rise, albeit at a slower pace compared to one month ago.

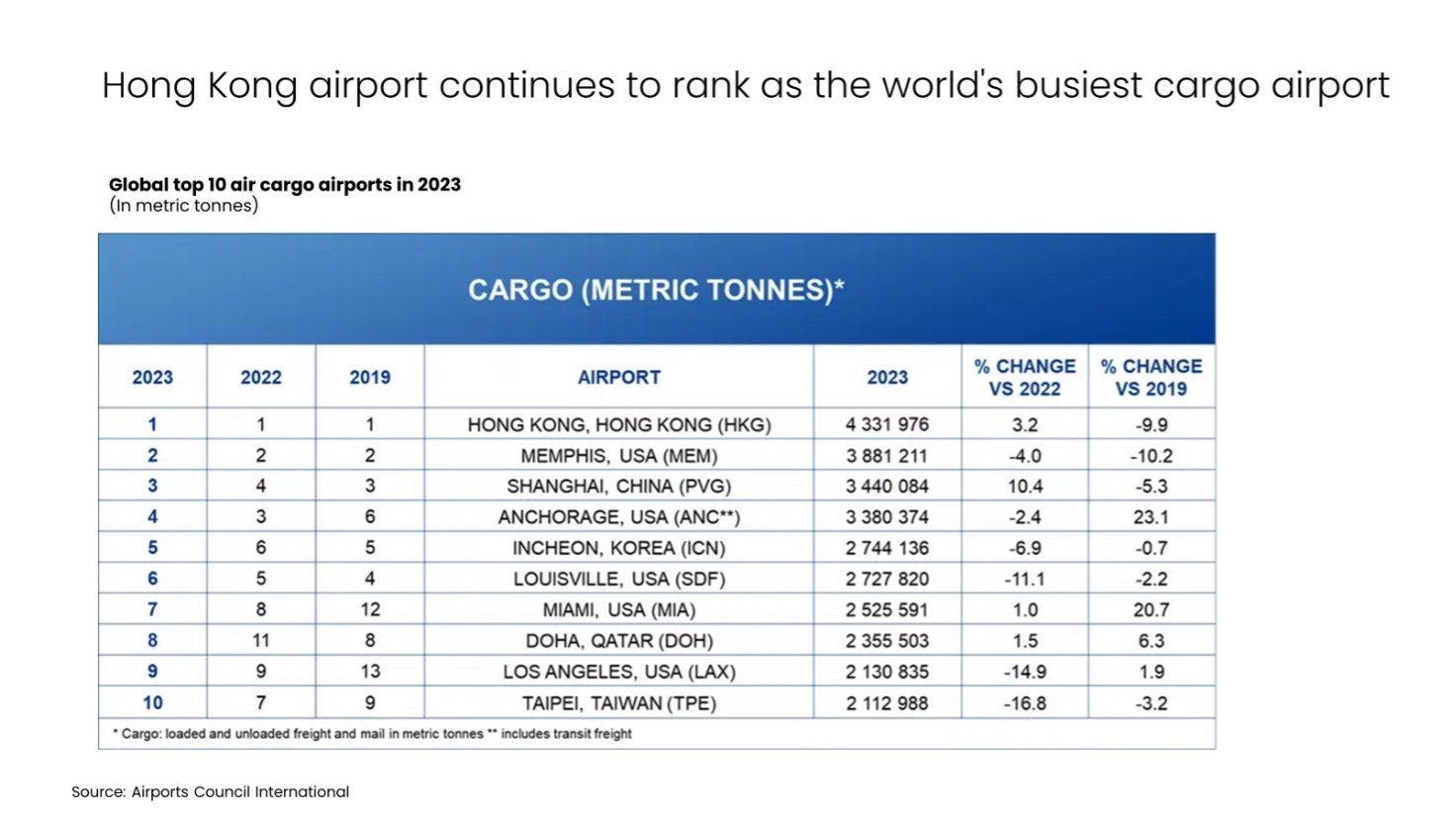

The world’s top 10 busiest cargo airports

The Airports Council International has released its 2023 ranking for the top 10 busiest cargo airports globally.

Hong Kong International Airport retained its position as the world's busiest cargo airport. Thanks to the easing of its Covid-19 restrictions and a boost from e-commerce, Hong Kong handled 4.3 million tonnes of cargo in 2023, up 3.2% year-on-year.

Shanghai Pudong International Airport also saw a significant growth in volume, increasing 10.4% year-on-year to 3.4 million tonnes in 2023. This allowed it to reclaim third place in the rankings, which it briefly lost in 2022.

Miami (ranked 7th) and Doha (8th) airports showed modest growth of 1.0% and 1.5% respectively, while the remaining airports in the top 10 experienced volume declines in 2023, namely Incheon (5th), Taipei (10th), and the US airports of Memphis (2nd), Anchorage (4th), Louisville (6th) and Los Angeles (9th).

Weaker parcel volumes from FedEx and UPS were the main reasons behind the declines at US airports.

AIR OBSERVATION

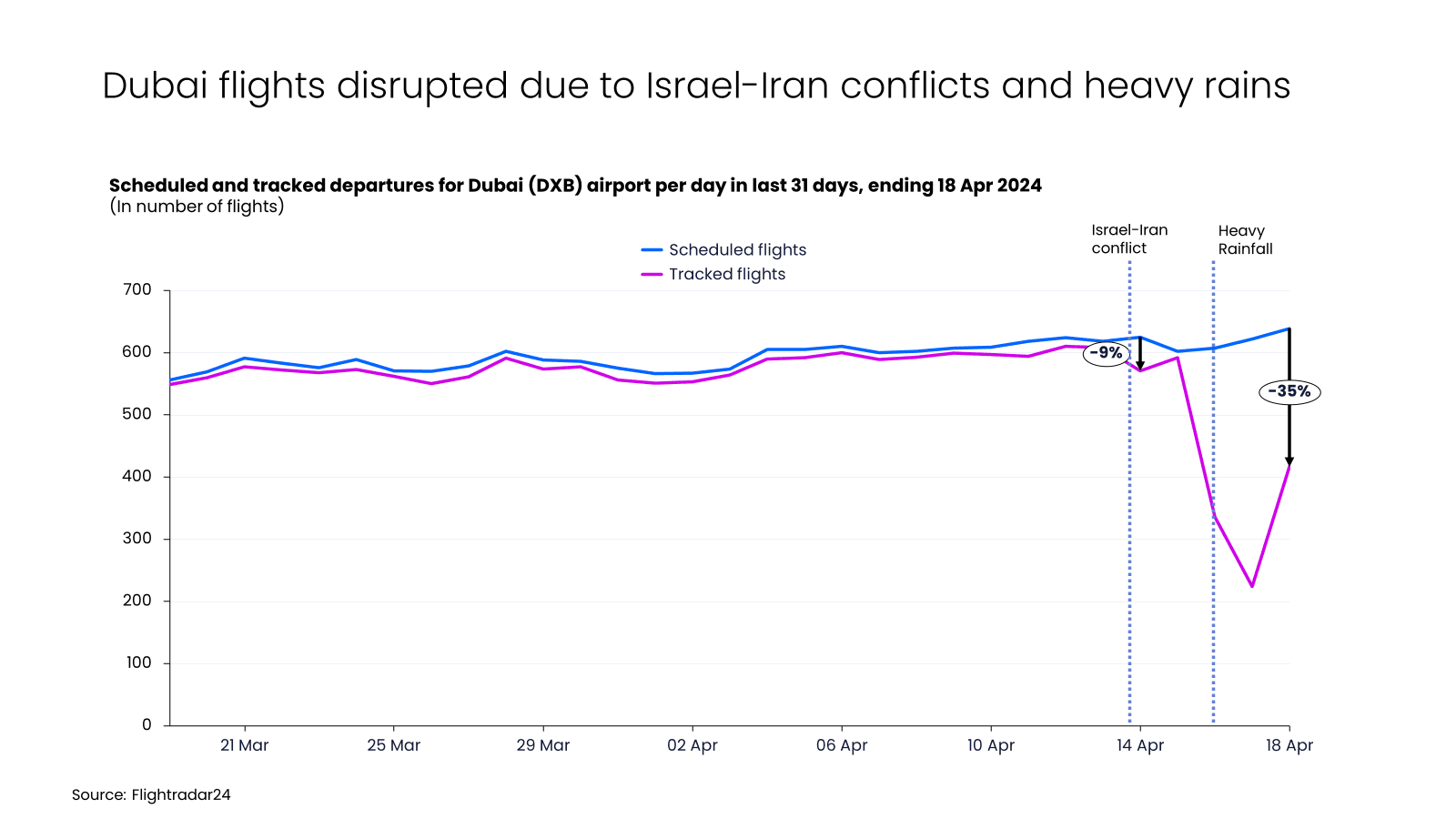

Dubai Airport, which is ranked among the world’s top 20 cargo airports, has faced a series of disruptions recently.

On Saturday, 13 April, missile and drone attacks by Iran on Israel led to the temporary closure of airspaces across Israel, Jordan, Lebanon, and Iraq. This resulted in the cancellation of about 9% of scheduled departures at Dubai Airport the following day, while some carriers opted to reroute to avoid the region.

It was not just air freight affected by conflict in the Middle East. In the early hours of 13 April and prior to the drone attacks against Israel, the MSC Aries ocean freight container ship was seized by Iranian forces near the Strait of Hormuz, a gateway to the Arabian Gulf and Jebel Ali.

This raised concerns regarding risk to ships sailing through the Strait of Hormuz, and in particular the potential impact on sea-air freight services.

Dubai is important hub for sea-air

Since the escalation of conflict in the Red Sea in December last year, Dubai Airport has become a key hub for sea-air freight services from Asia to Europe.

Cargo arrives in the Arabian Gulf from the Far East via ocean freight container services before being flown from Dubai to onward destinations in Europe and North America.

This has led to a near tripling (+190%) of air cargo demand from Dubai to Europe in March compared to the same month in 2023.

For the first two weeks of April, demand remained 146% higher than during the same period the previous year.

If there is a further escalation in the Middle East which compromises ocean freight container services from accessing ports in the Arabian Gulf it may potentially prompt a complete shift from ocean to air transportation for some shippers.

War-risk premiums and surges in jet fuel prices due to potential increases in crude oil prices could also occur, as was witnessed at the start of the Russia-Ukraine war.

However, this has so far not materialized, in fact the price of Brent crude oil only temporarily stayed over USD 90 per barrel on the Monday following the incidents on 13 April before falling below USD 90 by the middle of the week.

Then, following a further missile attack by Israel on an Iranian target, the Brent crude price increased 3% on 19 April from the previous day, nearing USD 90 per barrel.

The recent volatilities in crude oil prices reflect market uncertainties with the Israel-Iran conflict.

But as the crude oil price fell below USD 87 per barrel on 22 April, it demonstrates also that the oil market does not yet see any immediate risk to crude oil supply at this point.

Floods in Dubai add to disruption

On Tuesday, 16 April, record rainfall further disrupted Dubai Airport's operations. According to Flightradar24, as of 18 April, 35% of scheduled departures were canceled (source: Flightrader 24).

While rainfall is temporary, the knock-on impact of disruption caused by flight cancellations and missed connections at Dubai Aiport could linger for about a week due to the tight capacity situation which already existed prior to the downpour.

Escalation in conflict in Israel and Gaza in October last year and subsequent crisis in the Red Sea in December has raised fears of a regional spillover across the Middle East and recent events will serve to heighten some of those concerns.

For example, as well as an increase in Brent crude oil spot prices on 19 April, flight services to Tehran, Isfahan and Shiraz in western Iran have been suspended (source: BBC).

It is not possible to predict the trajectory of such a politically volatile situation with any degree of certainty, however, the escalation in conflict is adding further complications to already disrupted supply chains, particularly between Asia and Europe.

A look at freight forwarders' tender strategy

Uncertainties in the Middle East may prompt freight forwarders to prioritize securing capacity rather than pursuing lower rates ahead of this year’s peak season and any potential further escalation in conflict.

Early signs of this trend can be seen from regional spot share developments (the proportion of airline-sell volumes in the spot market).

In the first two weeks of April, 42% of global air cargo volumes were procured by freight forwarders in the spot market.

This is down 5 percentage points from the same period in 2023, but still 10 percentage points above the pre-pandemic level in 2019.

Instead, freight forwarders are looking to lock into seasonal rates, which in the first two weeks of April remained 5% below the levels in the same period in 2023.

This is in contrast to 5% growth in global spot rates when comparing against the same period.

Spot share declines

At an individual trade level, major fronthaul corridors experienced high single-digit or low double-digit declines in spot shares.

Forwarders on the Asia Pacific to Europe corridor allocated the least volume (40%) in the spot market in the first two weeks of April (this is still 10 percentage points higher than pre-pandemic levels of 2019).

The Asia Pacific to North America market had a 45% spot share in early April.

This was a considerable 12 percentage point drop from the same period in 2023 and on par with pre-pandemic levels.

This may well be a case of freight forwarders looking to secure capacity in anticipation of a continued e-commerce boom.

The spot shares for outbound Middle East and Central Asia (including the Indian subcontinent) to North America and Europe corridors remain high.

Despite a year-on-year double-digit decline, soaring freight spot rates have made some freight forwarders reluctant to lock more capacity into longer term agreements at high rates.

The Europe to North America corridor saw the smallest spot share adjustments in April compared to last year. Freight forwarders procured nearly half of the market volume in the spot market, which is up by 19 percentage points on pre-pandemic levels and suggests an anticipation of freight rate declines.

AIR OUTLOOK