Air Market News By Xeneta

March 22, 2024

Market News by Xeneta March 22, 2024

Visit Xeneta Customer Portal

(IQ Hub) For

Exclusive Market Content

The Xeneta Air iXRT provides an overview of market movements, the key risks and issues to be aware of and insight on how these may develop in the coming weeks and months. This is the first dedicated Air edition of the iXRT report. The first edition dedicated to ocean was published on 7 March.

Topics covered in this edition of the iXRT Air include:

Average global air cargo spot rates on the rise.

Red Sea conflict sees shippers switch from ocean to air.

Middle East and South Asia to Europe spot rate jumps a remarkable 51%.

Freight forwarders post 2023 results – and volumes are down.

Shippers leaning towards shorter contracts amid market uncertainty.

Summer schedules bring some classic seasonality.

Europe-US corridor set for drop in rates.

AIR RECAP

Contrary to the usual seasonal downturn, the average global air cargo spot rate in the first two weeks of March increased by 3% month-on-month from February, at USD 2.35 per kg.

This rise in the average global air cargo spot rate occurred despite a drop in jet fuel spot prices. The US Gulf Coast jet fuel spot rate was USD 2.617 per gallon in the week ending 15 March according to the EIA, a 5% decrease from four weeks earlier and just 1% above the same week in 2023.

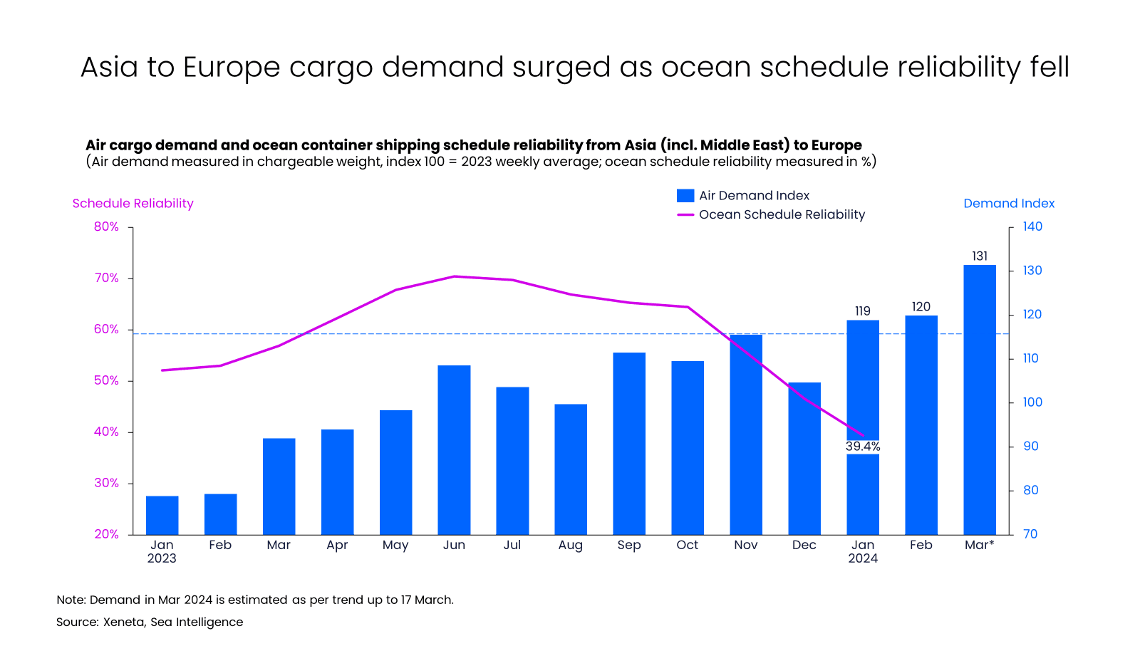

Many people will recall the demand hikes of Covid-19 when many shippers turned to air cargo due to unreliability in ocean freight services. The market is once again experiencing a shift in transport mode, this time around the disruption has been caused by ongoing conflict in the Red Sea.

As the reliability of ocean containerized shipping schedules dropped below 40% in January due to the disruption in the Red Sea region (source: Sea Intelligence), the average air cargo demand from Asia and the Middle East to Europe in the two weeks ending 17 March increased significantly.

This cargo demand was 31% above the average weekly level of 2023 and marked the third consecutive month of growth, surpassing last November's peak season high.

As a result, air cargo rates in the impacted region saw a substantial month-on-month increase.

In the first half of March, the growth in freight rates was led by the Middle East and South Asia outbound market.

Notably, the average air cargo spot rate from the Middle East and South Asia to Europe jumped a remarkable 51% to USD 2.60 per kg in the first two weeks of March, compared to the same period a month earlier.

Furthermore, given that European airports often function as transit hubs for the Middle East and South Asia, air cargo rates from the Middle East and South Asia to the US also experienced notable growth.

The average spot rate to the US was USD 3.63 per kg, a 26% increase month-on-month in the two weeks ending 17 March.

All of the top global air freight forwarders have now reported their annual results for 2023.

Despite an increase in cross-border e-commerce volumes driven by consumer demand in Europe and US for low-value goods, manufacturing activities failed to deliver meaningful growth in overall air cargo demand.

Looking at the top three air freight forwarders, K+N, DHL and DSV all reported negative year-on-year growth in air cargo volumes for all quarters of 2023.

In Q4 2023 specifically, K+N reported the smallest volume decline of 2% year-on-year, followed by a 4% decline from DHL, and a significant 8% decline from DSV.

AIR OBSERVATION

As a result, the gross profit per unit reported by these top three forwarders also declined year-on-year in Q4 2023, namely DHL by 43%, K+N by 32% and DSV by 19%.

The volume figures from Q1 2023 may also explain the double-digit growth in global air cargo demand in the first two-and-a-half months of this year.

This growth, while clearly significant, must take into account it is rising from a relatively low base established in Q1 2023.

Therefore, rather than being a surge in demand, 2024 global air cargo volumes could instead be viewed as a recovery from the lower levels of demand in 2023.

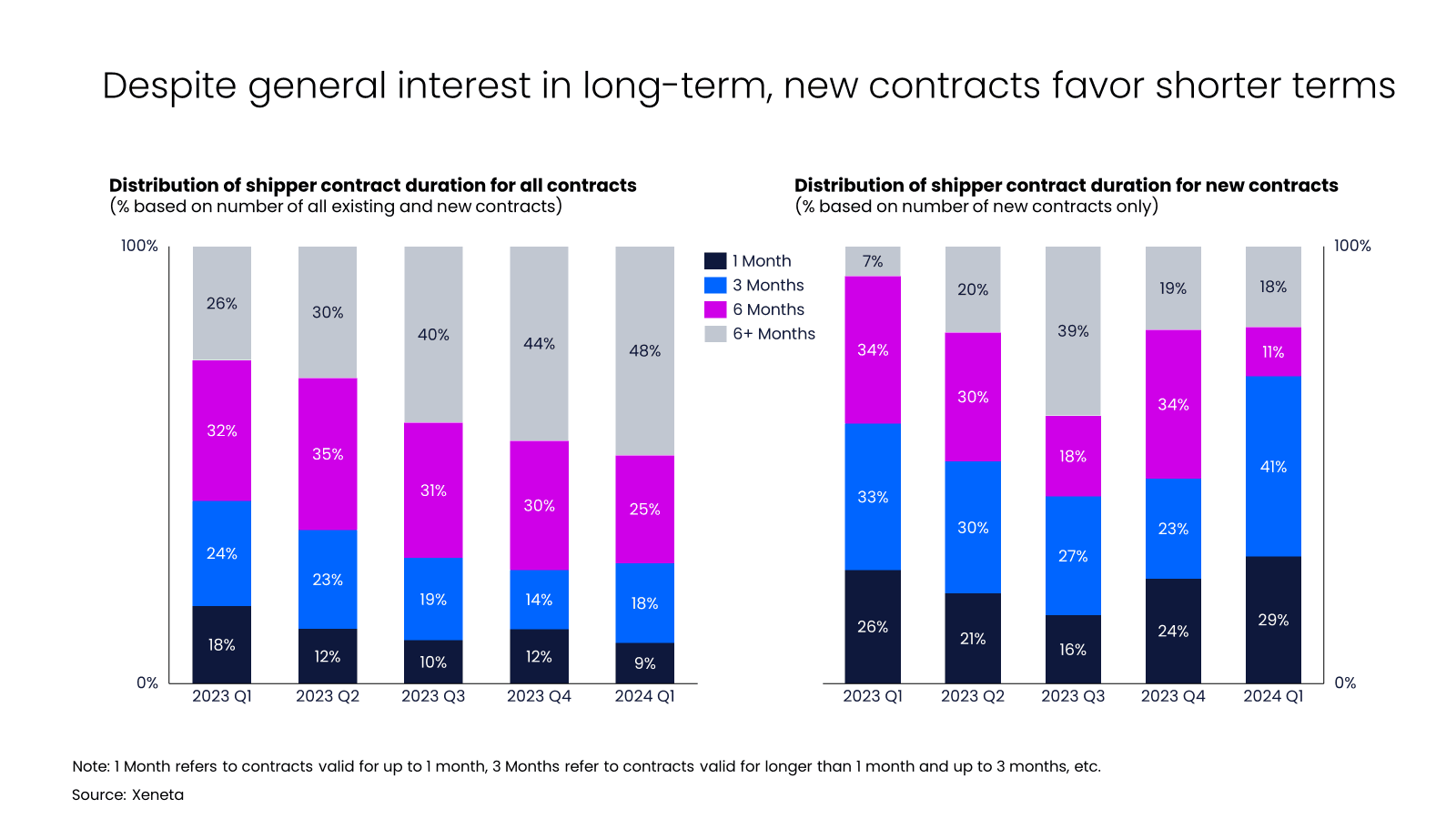

With tender season for new contracts under way, the recent market developments have left many shippers with difficult choices.

Many new contracts are set to begin in April and shippers have remained cautious over whether they should agree a new deal or attempt to extend their existing agreement.

If they decide to enter a new contract, how long should it last given the market could look very different as we head further into 2024? Three months? Six months? One year?

Xeneta data for Q1 2024 suggests shippers have been veering away from longer-term contracts, possibly so they can see how the situation in the Red Sea develops.

For example, in Q1 2024, contracts over six months account for almost 50% of all valid contracts in the market.

However, when we look at newly-signed contracts in Q1 2024, agreements over six months account for just 18%.

Meanwhile, the share of three-month contracts signed in Q1 2024 has increased to 41% from just 23% in Q4 last year.

It is clear our customers are using the Xeneta data and intelligence platform to monitor the market very closely.

And who can blame them? With air cargo rates still on the rise, it might not be the ideal time to lock into longer term contracts, particularly for routes transiting via the Middle East.

Shorter contract lengths with rate reviews every three months (or postponing negotiations completely) appears to be the more prudent option.

Despite all the uncertainty, there is still some classic seasonality in the market with airlines’ summer schedule set to commence on 31 March.

This will impact the market between Europe and North America the most due to an influx of belly capacity as summer travel in the northern hemisphere picks up.

This air freight corridor will see approximately 33% in additional cargo capacity from March to its peak in June.

As a result of this additional belly capacity, air cargo rates between Europe and North America will likely drop.

Potential beneficiaries of this situation are the India and Southeast Asia regions because shipments from these countries frequently transit via Europe en route to North America.

AIR OUTLOOK

Xeneta is the leading ocean and air freight rate benchmarking, market analytics platform and ocean container rate index, Xeneta Shipping Index (XSI®).

Xeneta’s powerful reporting and analytics platform and data density provide liner-shipping stakeholders the insights they need to understand current and historical market behavior – reporting live on market average and low/high movements for both short and long-term contracts.

Xeneta’s data is comprised of over +400 million contracted container rates and covers over 160,000 global trade routes. Xeneta is a privately held company with headquarters in Oslo, Norway and regional offices in New York and Hamburg. To learn more, please visit www.xeneta.com

NOTE: The XSI® public indices reports are based on long-term contracts only.

© 2024 Xeneta AS

Long term rates contracted within last 3 months